Small Cap Idea: Rover (ROVR)

Marketplace for the price of a melting ice cube

![[redacted]'s avatar](https://substackcdn.com/image/fetch/$s_!lWn2!,w_108,h_108,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F17d07f92-f7cb-4c47-8487-c12ee130769c_3419x3021.jpeg)

****Update (November 29, 2023): Rover to be acquired and taken private by Blackstone for $11.00 per share. This is a premium of ~61% to the VWAP over the previous 90 trading days, and ~160% above the stock price of $$4.23 when this report was published.

We want to acknowledge that this idea originally came from a good friend of Value Punks - Panoramic Capital. Panoramic is a skilled investor focused on small and micro-cap ideas. He was recently a portfolio manager at a large institutional manager. Give him a follow!

*** Our previous small cap idea Diversey Holdings (DSEY) was acquired and taken private in March, two months after we published our report, at 93% premium to our cost base ***

Rover is the world’s largest network of pet sitters and dog walkers. Rover connects pet parents with pet care providers who offer overnight services, including boarding and in-home pet sitting, as well as daytime services, including doggy daycare, dog walking, and drop-in visits. The marketplace has more than 500,000 pet care providers across North America and Europe.

Rover is listed in the US and is currently trading for $4/share and has a market capitalization of $750 mn with $250 mn in cash for an EV of $500 mn. The company reported revenues of $174 mn and adj. EBITDA of $20.8 mn for FY22 ending December 2022. At the midpoint of its guidance for 2023, it should do $210 mn in revenues and $27.5 mn in adj. EBITDA. This means that this dominant marketplace is trading for EV/adj. EBITDA of 24x for FY22 and 18x for FY23.

This does not sound that cheap? Did Value Punks just become Growth Punks?

No! As we will argue in this report, Rover is under earning. It has the potential (and LT management guidance) to achieve 30% plus adj. EBITDA margins. In fact, most marketplaces have very high margins as all they do is essentially collect a toll without a need to have any assets. As a marketplace grows, the two biggest expense items are (a) demand generation, and (b) supplier incentives. Once the marketplace gets going, both these expenses can be throttled back and the real economics of the business come through.

With Rover, if we assume ‘look through’ margins of 30% then it should have $63 mn in adj. EBITDA in 2023 on $210 mn in revenues. At that level, it is trading at 8x fwd EV/adj. EBITDA.

Now that is cheap for a dominant marketplace with a recurring revenue business!

Introduction

Rover was started in December 2011 by three dog lovers in Seattle’s tech scene. Greg Gottesman, who spent 20 years as a venture capitalist, came up with the idea after his Labrador was mauled at a local kennel. He recruited Microsoft’s former general manager Aaron Easterly to be Rover’s CEO, and Philip Kimmey to be the company’s director of software development.

In 2020, Rover came public through a SPAC led by True Wind Capital (ex-KKR). It was a successful SPAC in the sense that it infused Rover with a lot of capital but like all SPACs in 2022, the stock has discriminately sold. The business was also heavily affected by Covid which resulted in fewer people traveling and thus needing less pet-sitting services.

Today, Rover is the largest peer-to-peer marketplace business that connects pet parents with service providers. The platform is full featured. It handles everything from search, booking, chat, and payments. Rover generates revenue by charging a booking fee to pet parents and a take-rate to service providers.

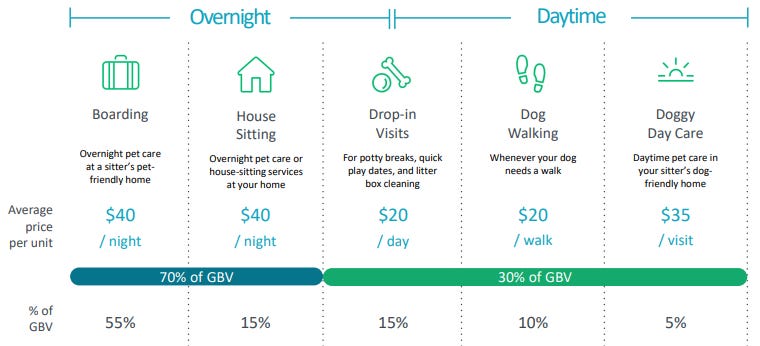

While the platform allows for a variety of pet related services, the majority of the gross booking value comes from overnight bookings, as shown below.

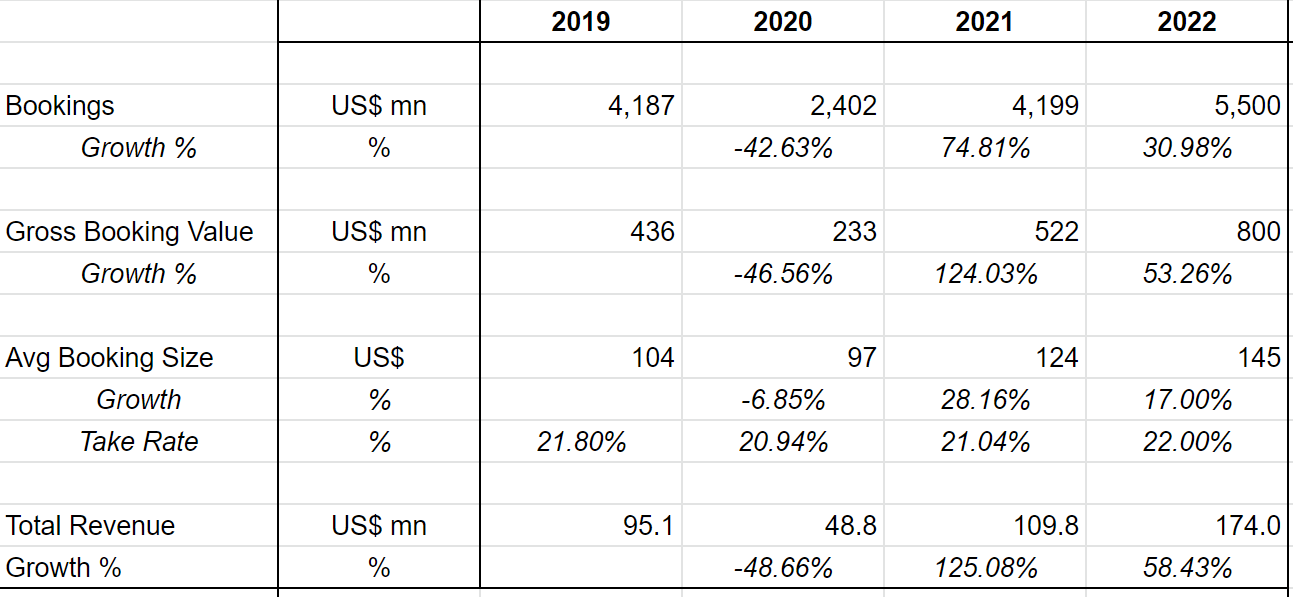

In FY22, with the Covid-related issues in the rear view mirror, Rover has been beating expectations and firing on all cylinders. This is how the business evolved over the last 4 years:

In any technology business one has to be confident that the management is focused not just on growth, but also profitability.

“Aaron, the CEO, is an economist. Brent, the COO, who was my boss for a period of time there is very analytical and also big economics background. I think sometimes that serves the business really well, but it also made it hard to invest in longer-term plays because we were always so worried about the unit economics tomorrow.”

-Rover, Director of Product Management, Sept 22 - Stream Transcript

It is interesting because typically, one would expect the opposite out of a SPAC/tech company. Most of them neglect unit economics while claiming that they are maximizing for long-term growth. Rover is different. It’s a financially well-managed technology company.

Business Quality

A two-sided marketplace is a wonderful business model. We argue below that Rover is a high quality business that meets the tests above of a successful marketplace.

We will go through some of the important points below:

Rover is a high quality marketplace business

Fragmented demand and supply: Rover sits at the center of a very fragmented supplier and user base. As of 2022, Rover connected ~1m+ pet parents, to more than 320k service providers. 98% of service providers are non-professionals that are doing it to earn a bit of extra income (~$2.2k/yr on avg).

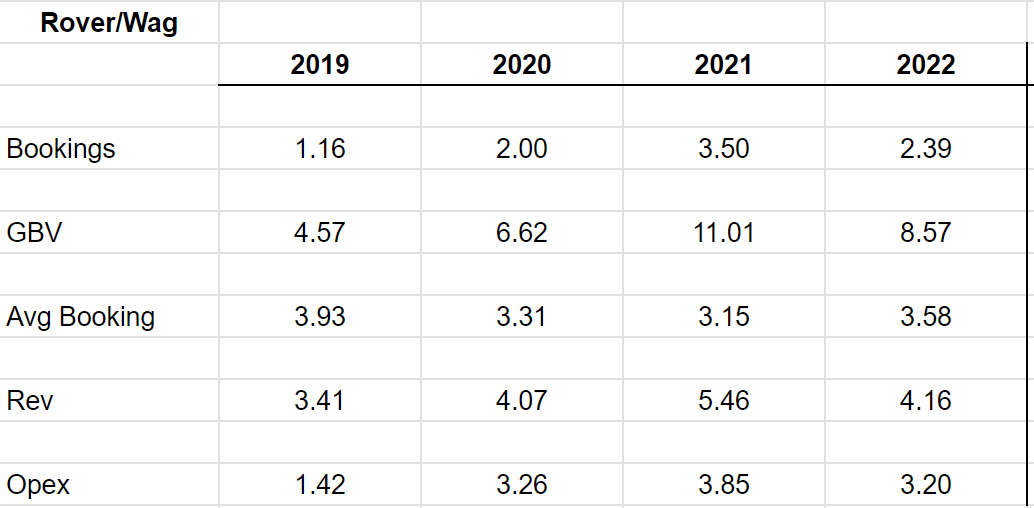

Dominant: Rover is “the” marketplace for pet sitting. The company’s closest competitor is Wag!, whose GBV is <1/8th of Rover’s. Wag! is also a business that is focused on on-demand dog walking (lower TAM/ASP) vs overnight boarding.

No good alternatives: Neither pet parents nor service providers have good alternatives.

Think of it this way: For pet parents, Rover is akin to AirBnB for pets…if OTAs didn’t exist (Wag! is the only other website); hotels were like prisons (look up photos of kennels); and the only alternative was to beg your parents or friends to let you stay with them.

Even if you have a willing friend/family member, they need to live somewhere that can accommodate your pet, and be free the entire time you’re gone. You’ll also feel awkward sending specific care instructions to someone doing you a favor. (Ever tried asking your in-laws to brush your dog’s teeth every night?)

For service providers, while there are alternate advertising channels available, it will be much more difficult to find pet parents who are willing to pay you to board their pets (issue of trust)

In essence, this network effect becomes the moat:

“You need heavy supply before you can even consider pricing. And the reality is if you have a very limited supply of pet service providers, you're not going to be able to even come close to competing on a pricing front. And that is just the first barrier to entry. It is pricing. People care about experience, safety, credibility, all those things, which just comes with volume.”

No labor issues: Unlike Uber or Doordash, Rover doesn’t rely on the “gig economy”, and doesn’t face similar labor issues.

Rover is growing very quickly, with a long runway ahead

Rover is still in its fast growth phase. For FY22, its grew revenues 58%.

In 2023, growth will decelerate. Management’s 2023 guidance implies 21% revenue growth (an estimate that we think they will beat). FY22 growth included quite a bit of average booking value growth, due to service providers raising prices in line with inflation. Nevertheless, booking volumes are still growing at high teens+ rates, and saturation point seems long way off:

90% of pet care is still provided by friends and family. While they will remain the primary choice, there’s plenty of room for Rover to grow while still being a “niche solution”

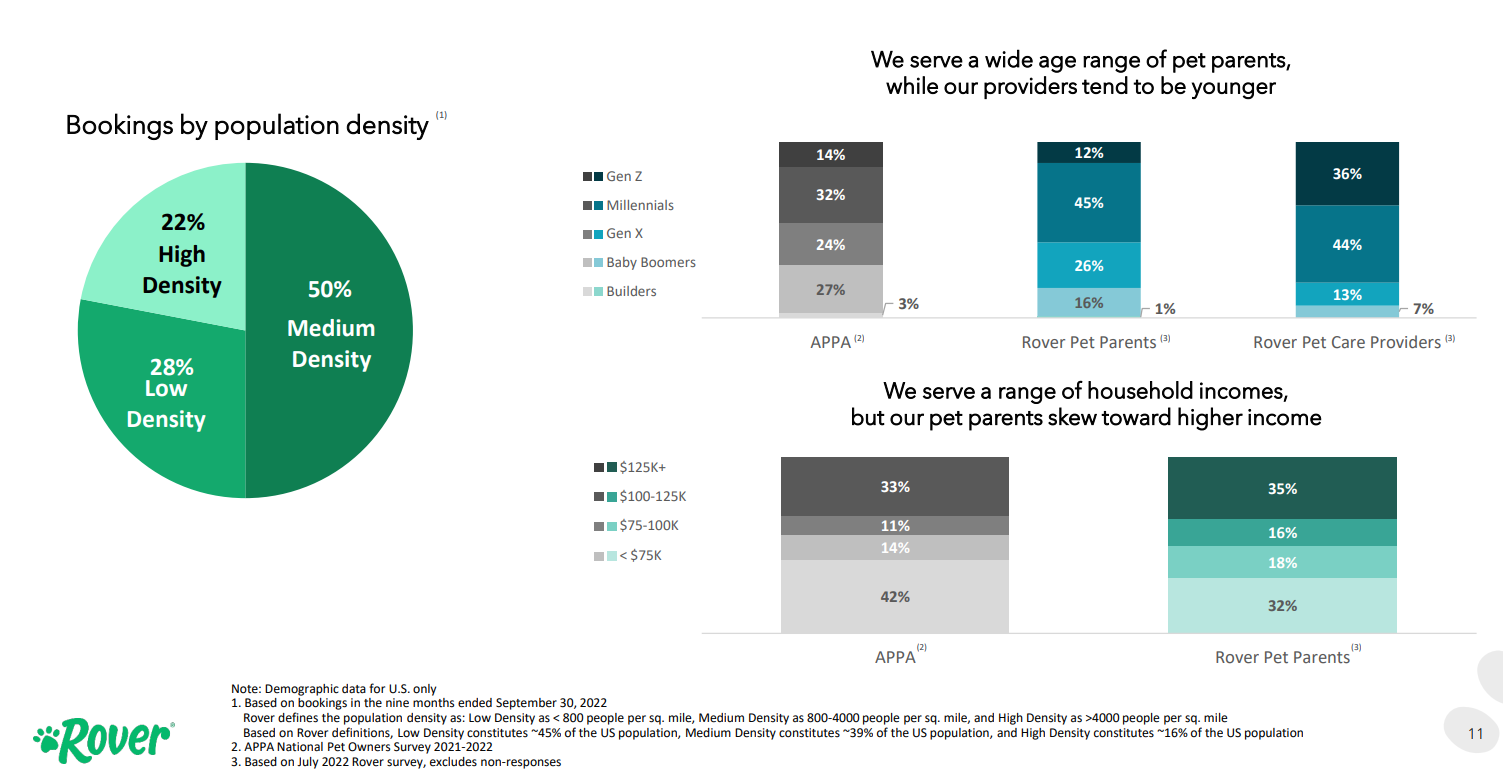

Rover’s services are broadly used across city, age, and income brackets, as per the slide below:

Rover launched in UK / Europe in 2018, and is currently growing at 100% YoY, albeit off of small base.

Economics of a mature, dominant marketplace business is extremely attractive

High-value add marketplaces with dominant market shares are essentially license to print money, for a few reasons:

High gross margins: marketplaces don’t really “sell” anything - it’s a media business, and as such, typically sport very high gross margins.

Simple operations with high operating leverage. Marketplace businesses are simple operations. Once you become “the place to go”, you just have to maintain the status quo. A hallmark of a great marketplace business is that marketing costs decline rapidly as you become the dominant player, as network effect ensures that buyers and sellers naturally gravitate toward the platform. This is shown below:

Pricing Power: There’s fair bit of pricing power. As the only player in town, you can charge high prices for using the platform. An as example, competitor Wag! has a take rate averages in the 40% and reached a high of 60% in Q3! This is double and triple Rover’s 22%.

Rover exhibits all of these features. Gross margins are high (75-80%), marketing costs are falling rapidly, with a strong source of “free” customer acquisition and we’ve seen fixed costs such as G&A and R&D costs start to fall as % of revenue recently.

The company is currently at 10% adj EBITDA margins and is aiming for 30%+ EBITDA margins. We think it can do a lot higher. Check out these EBITDA margins for other, mature, dominant marketplace businesses.

Rightmove, UK property portal: 75%

Hemnet, Swedish property portal: 54%

Adevinta France, a general classified site: 47%

AutoTrader UK, UK used car marketplace: 71%

Whatever the number ends up being, Rover is very likely to be a highly profitable business. As mentioned previously, given the quality, growth, and potential margins, Rover is trading at a very low price today. A dominant marketplace that is inflecting on margins should trade at a much higher valuation. We believe the current valuation of 8x ‘look through’ adj EBITDA will prove to be very cheap in hindsight.

It seems like the management agrees with us and has instituted a $50 mn buyback program which should support the stock price in a highly volatile market environment.

Risks

1.) Competition

Wag! is a small but fierce competitor. It has gone through various phases in its life including a phase where it was funded by Softbank which encouraged it to ‘go for it’. Wag! too came public via a SPAC - but in 2022 when it was a little too late; due to this, the SPAC could not raise any capital as it came to the market and had some debt to boot. While we think the management team here is competent, they have been dealt a very difficult hand.

In a marketplace, scale matters and Rover is clearly ahead of the game:

It is important to note that the above economics for Wag! are achieved by taking a 40-60% take rate. This is almost double Rover’s 22% take rate. To further emphasize, Wag! takes $40-60 for every $100 transaction while Rover takes $22. While this can temporary boost profitability (which they need to service their high cost debt), we believe this is to the detriment of long term profits and business sustainability. We believe the management at Wag has not read Bill Gurley’s seminal work on take rates - A rake too far: optimal platform pricing strategy.

What is more important is that it increases the risks of disintermediation:

“But once you've built up that relationship and your dog built that relationship with that other human, we found anecdotally that pet parents were much more comfortable just being like, "Yeah, let's take this offline." And when also pet parents found out that Wag was taking 40% of every service that they were paying we also found pet parents were surprised by that.”

Unlike Rover, Wag! has a different business model:

“People associate Wag with on-demand. Think of it as like an Uber. You need a service. Who's the quickest person? When can they get here? Versus Rover, which was traditionally associated with more of a Yelp kind of marketplace, where you are going to source things not necessarily on demand”

In essence, with the Rover model, a pet parent has control and with the Wag! model it is an algo matching the pet-parent with a caregiver. We think Rover has clear advantages in this industry:

“I think with sitting and boarding, the control aspect made sense because I think there is really no need for on-demand sitting and boarding unless it's like an emergency. And sitting and boarding is usually for a lot longer time than like a 20, 30-minute walk. And so the risks of you putting your pet in the hands of a stranger for that amount of time are just inherently greater than you trusting a stranger for 30 minutes to take your dog on a walk.”

There is currently a large gap between Rover and Wag!’s take rates - we see it as a free option for Rover to incrementally and strategically take its take rate up over the next few years.

2.) Travel-dependence

Rover’s revenue model is bookings driven. The main driver of its services is vacation related travel.

If we hit another lengthy mass travel disruption event in US, it’s going to be ugly.

3.) Margin achievability

While theoretically, Rover should be highly profitable, this depends on management’s spending discipline and shareholder treatment. The company is currently ramping up margins, and it’s hard to imagine Rover blowing through its balance sheet right after coming out of COVID. Nevertheless, as much of the spending is discretionary, we won’t know what mature margins look like until we get there.

SBC is definitely a factor when considering terminal margins. The company reserved 17m shares (<9% of shares outstanding) for its 2021 equity incentive plan and ran through about 60% of it in the last 7 quarters, so overall dilution isn’t a deal breaker, but something to watch out for.

4.) Service provider onboarding and churn

Disintermediation, where a pet owner and pet care provider transact offline becomes a risk. While Rover isn’t a gig economy company, it still relies on a new breed of suppliers - those that are willing to take care of other people’s pets for a bit of extra income. Rover has to create supply by onboarding service providers. Unfortunately, Rover does not report supplier churn numbers. However, this is expected to be high. Rover notes that over 800k care providers have been paid, with there being 320k active providers today.

Conclusion

Rover is the leading pet services marketplace in the US, Canada, and Europe. We know that people love their pets. This pet ownership has grown on a secular basis including during periods of macro weakness - the US pet industry grew during the 2008-10 recession.

Rover is the clear category leader with ~10x+ more scale than its closest competitor, and possess the attributes of a high quality marketplace business. Rover turned profitable in 2021, and in our view is well positioned to drive significant profit growth through operating leverage. There are also a number of growth opportunities such as international expansion and new service/pet offerings that are worth watching for.

When we combine the above with low valuations and a net-cash balance sheet, we find a stock with the ability to compound at attractive rates.

Disclaimer: The author(s) own Rover shares.

If you are looking for an expert network to get up to speed on industries and companies, then we highly recommend Stream by Alphasense.

Stream by Alphasense is an expert interview transcript library that has been integral to our research process. They are a fast growing expert network with over 25,000 transcripts on a wide variety of industries (TMT, consumers, industrials, real estate and more). We recommend Stream for its high quality transcript library (70% of experts are found exclusively on Stream) and easy-to-use interface. You can sign up for a free trial by clicking here.

I struggle to see how/why a customer/supplier can't just cut out rover in this arrangement over time if it is a recurring service they are providing? It seems like a good source for new leads but once they get that direct relationship why not just be like hey can you just pay me directly instead of through the platform. what am i missing?