Peloton: Survival of the Fittest

Patent Filings and Other Moves Wall Street Is Missing

“I once described turnarounds as a full contact sport: intellectually challenging, emotionally draining, physically exhausting, and all-consuming … From where I sit today, that pretty much summarizes my experience these last two years … A lot of blood, sweat, and tears have been shed to make Peloton’s turnaround possible … I’ve done my very best to recruit a truly talented exec team to lead the turnaround. If I have one lasting legacy at Peloton, it will be this: You have a GREAT lead team, and although the stock market hasn’t recognized this yet, it will. It’s simply a matter of time.”

– Former CEO Barry McCarthy, final memo to employees, May 2nd, 2024

Introduction

Peloton’s stock has rebounded following its recent earnings report, but McCarthy’s message remains pertinent. Investor sentiment is slowly recovering, though short interest is still elevated at around 18%, a modest 2% drop since the earnings announcement. This analysis arrives a bit later than intended (due to a major project for The Globe and Mail, coming soon), but if accurate, Peloton’s current valuation presents an appealing asymmetric risk-reward opportunity.

In his final earnings call, McCarthy stated, “If you look at our balance sheet, you’ll see that the business is not going away, which for a long time was a systemic threat. So, because of that, we’re able to focus on renewed growth… I think you’re going to see significant product innovation over the next two years, which I’m very excited about because we have a real shot at changing the growth trajectory of the business.”

Hardware Innovation

Peloton has indeed been quiet on the innovation front, particularly in hardware—until now. Historically, the company has kept product development under wraps for competitive reasons, as CFO Liz Coddington recently reminded investors. But patent filings offer a glimpse of what lies ahead. After extensive scrutiny, some intriguing details have emerged.

The third iteration of Peloton’s iconic bike appears to be nearing release. While the current model has aged gracefully, a decade without significant updates is starting to show. Our research confirms that the V3 Bike is in development, promising more than just incremental improvements.

The more significant breakthrough, however, may come from Peloton’s treadmill lineup. Historically an underperformer—Peloton has sold ten times more bikes than treadmills—despite the treadmill market being two to three times larger. Recent patent documents hint at potential disruptive innovations. If approved, even with narrower claims, the long-term potential could be substantial.

Uncertainty remains, of course. The patent process is complex, and our investigation into related filings has been exhaustive (and occasionally tedious). Most of these details are consigned to the footnotes.

Digital and App Innovation

Peloton’s recent digital efforts show promise, particularly in personalization, gamification, and the launch of a standalone app. These initiatives could boost subscriber growth, increase engagement, and reduce churn.

Leaning Toward Hardware Agnosticism

Peloton estimates that over five million treadmills and bikes are sold annually in the U.S., mostly at lower price points. Yet its robust digital platform—with a near-perfect 4.9-star app rating—offers a pathway to attract more customers who either cannot afford or prefer not to own its hardware.

The Myth of Market Saturation

The notion that Peloton is approaching market saturation is flawed. Data suggests otherwise: unaided brand awareness is surprisingly low across most of Peloton’s product lines, except for the Bike, which has roughly 57% awareness in the U.S., but significantly lower internationally. Awareness of Peloton’s treadmills in the U.S. sits at 20%, while the app and Row have even lower recognition at 6% and 4%, respectively.

As explored later, awareness often does not translate to deep product understanding. Many consumers overestimate Peloton’s cost while underestimating the quality, variety, and overall user experience, making saturation claims premature.

Consensus Remains Conservative

Management’s FY25 guidance does not incorporate potential gains from digital initiatives, and consensus estimates are similarly conservative. Analysts expect flat revenues in FY26, but even modest digital success could see Peloton exceed expectations. This is before factoring in an innovation-driven hardware sales cycle, likely to commence by FY26.

Conclusion

Peloton may not meet the traditional definition of a “value” stock, but our analysis suggests that it presents a compelling asymmetric risk-reward profile over the long term. If directionally accurate, Peloton could substantially reduce its debt over the next three years, with a clear path to positive operating income by FY26 and meaningful gains thereafter. This view differs significantly from consensus, which justifies some skepticism. However, there is much about Peloton that remains misunderstood, both within and beyond the investment community. As we delve deeper, these misunderstandings should become clearer.

Here’s what else we’ll explore:

The company’s increasing commercial traction, marked by key partnerships with Google and Hyatt—the latter particularly intriguing.

McCarthy’s assertion that Peloton now boasts a “GREAT lead team,” why it represents the strongest lineup in the company’s history, and why this matters, especially in marketing and R&D.

The evolving competitive landscape, broader industry trends, and their implications for Peloton’s future.

Why Peloton’s efficiency has room for improvement beyond what recent restructuring efforts and public commentary suggest.

Barry McCarthy, whom we’ll introduce more fully soon, was instrumental in stabilizing Peloton. His blunt, no-nonsense approach was exactly what the company needed in a crisis. However, his style was more pragmatic than visionary—not surprising for a career CFO who was thrust into the CEO seat. Now, Peloton requires a leader who can rally the company around a compelling vision, inspire employees, and excite customers.

It’s hard to miss the symbolism of launching a refreshed version of the bike that put Peloton on the map, just as the company prepares to announce a new CEO and turn the page to a new chapter. That leader could be revealed any day now, as interim co-CEO Karen Boone hinted during the last earnings call: “We’ve been very focused on it. We are far along in the process ... We’ve narrowed it down to some very highly qualified candidates ... I should probably under-promise here, but I believe you’ll be hearing from the new CEO on this call next quarter.”

Disclosure: I’ve owned a Peloton for a couple of years, riding under the extraordinarily clever handle “WheeliamShatner” alongside my partner. While I’m not the typical Peloton enthusiast—the classes don’t quite grab me, and the “high-fives” feel more distracting than motivating—my partner is fully immersed in the community. This dual perspective offers a unique vantage point. I’ve experienced the product, engaged with the members, and closely followed the industry, giving me a clear lens on what truly matters—especially when it comes to innovation and how Peloton can better engage members like me (who, we suspect, skew male).

All figures are in USD, and all years refer to Peloton’s fiscal calendar unless otherwise noted. Some quotes may be lightly edited for clarity and flow.

History

In 2011, John Foley, a seasoned business executive and fitness enthusiast, found himself in a cycling class in Manhattan—ground zero for the boutique fitness craze. Just like in San Francisco, Los Angeles, and Seattle, high-end studios like Orangetheory and Barry’s Bootcamp were springing up everywhere, offering the latest must-have experience for the urban, smoothie-drinking, athleisure-clad crowd.

“… That’s where you want to be if you are an up-and-coming instructor in this burgeoning new category … there are so many great instructors at these places that have cult followings … it’s so hard to get spots in those classes. The instant they become available, you even had to do this in Seattle, I remember, but in New York it’s impossible.”

- David Rosenthal, the Acquired podcast

This experience sparked Foley’s game-changing idea: a connected stationary bike that would bring live studio classes directly into people’s homes. The value was clear—no need to live in a boutique hub like NYC to access top-tier instructors, no more scrambling for class slots, no steep per-ride fees, and—most appealing of all—class sizes that didn’t cap at 50. Unlike SoulCycle, there would always be room for one more.

But big ideas come with big risks, and investors weren’t exactly clamoring to buy in. Undeterred, Foley turned to friends and family, raising $400,000 through $25,000 and $50,000 checks at a $2 million post-money valuation. Capital may have been tight, but talent was easier to come by—Foley successfully convinced four co-founders to join him on the ambitious journey.

The team knew the bike couldn’t just be functional; it had to look good enough to earn a place in living rooms, bedrooms, or even offices—after all, most of the boutique crowd didn’t have home gyms. Over the next 18 months, they poured their efforts into prototyping what they envisioned as “the most beautiful bike ever designed.”

“There were a number of things we quickly realized we could improve on,” said Tom Cortese, Peloton co-founder. “For starters, bikes today are loud and clunky, so we threw out the chain. We replaced it with a belt drive—smooth, super quiet. You can ride at home without bothering anyone. We also got rid of the brake pads—it’s all magnets now, passing around the flywheel. It’s awesome.”

The search for their first instructors kicked off in May 2013, with the following ad:

In the summer of 2013, Peloton launched a Kickstarter campaign, setting the price of its bike at $1,500 and aiming to raise $250,000. They exceeded their goal, raising $307,000 from 297 backers. But the outcome wasn’t quite the home run they had hoped for.

“We launched a website at pelotoncycle.com and did some marketing on Facebook, but it was mostly crickets. We’d sell about five bikes a week,” Foley recalled. It became painfully clear that people needed to see and experience the product in person. That realization led to their first store opening at New Jersey’s Short Hills Mall in November 2013.

The success of that first store spurred them to open more in 2014, hire additional instructors, and run their first commercial. With the network effect kicking in, Peloton generated $10 million in revenue that year and secured its first institutional funding round, led by Tiger Global.

Momentum continued to build. By 2015, sales skyrocketed to $60 million, and in 2016, that number nearly tripled to $170 million. Peloton officially joined the unicorn club in 2017, raising $325 million at a $1.3 billion valuation. Then, in August 2019, Peloton filed its S-1 with the SEC.

When “PTON” debuted on the NASDAQ a month later, it ranked as the third-worst “mega-IPO” since the financial crisis. Still, this wasn’t exactly a flop—Peloton raised $1.16 billion at $29 per share, reaching the upper end of its target range. And then, on March 11, 2020, the World Health Organization declared COVID-19 a global pandemic.

Within six weeks, over 1.1 million people had downloaded Peloton’s app, and Q4 revenue surged 170% Y/Y. Demand for bikes and Treads soared to the point where customers faced months-long waits, and some resold their equipment at hefty markups. Peloton quickly became one of 2020’s standout stay-at-home stocks—a “pandemic darling.”

“COVID was the marketing campaign that Peloton never could have afforded. The growth that happened during COVID propelled the business to scale in a way that no other company has achieved. That afforded access to capital that it wouldn’t otherwise have and made it the dominant player in the connected fitness category.”

– McCarthy, from a December 2022 interview

As vaccines rolled out in late 2020 and gyms began to reopen, questions loomed about Peloton’s post-pandemic future. The stock peaked soon after, but Foley’s confidence never faltered. In February 2021, he boldly predicted, “We will continue to be a high- or hyper-growth company for years and years to come … you have to think about how you make millions of treadmills a year, three or four years from now … but not getting over your skis with fixed costs and overhead.”

Yet Peloton had already done just that. By early 2021, the company had increased manufacturing capacity by over 700% Y/Y, while also pouring money into retail showrooms, warehouses, last-mile delivery fleets, and a workforce that swelled from 2,000 employees in 2019 to over 8,500 in just two years.

“There is but one step between the sublime and the ridiculous,” Napoleon famously remarked during his retreat from Russia in 1812. Peloton’s own retreat from its pandemic highs echoes that sentiment. The cost of these largely self-inflicted missteps—restructuring, impairments, recalls, and litigation—topped $2 billion. Under increasing shareholder pressure, CEO John Foley stepped down in February 2022.

Enter Barry McCarthy, a no-nonsense operator with a sharp, analytical mind, best known for steering Netflix and Spotify through periods of rapid growth as CFO. As CNBC’s Gabrielle Fonrouge put it, “employees breathed a sigh of relief to have what felt like an adult in the room, someone who’d be able to clean up a multibillion-dollar mess.”

McCarthy summed up Peloton’s leadership failures by contrasting them with his former colleagues. “What makes Reed Hastings and Daniel Ek such great executives is that they deal with the world as it is, not as they want it to be … The Peloton team didn’t exhibit that capacity, right, to imagine that COVID was going to be the new normal.”

Operationally, the company was in disarray. The order management system, built on outdated code, caused headaches across departments, particularly in accounting and customer service, where employees had to navigate up to 16 different screens just to access a customer’s history. Engineers, too, were hamstrung, unable to push updates or efficiently run A/B tests. “We have to wait until the end of June to A/B test something that would take 1.5 days at Netflix,” McCarthy lamented.

To right the ship, McCarthy transitioned Peloton to a variable cost model, exiting in-house manufacturing, outsourcing logistics, scaling back retail, partnering with Dick’s and Amazon, and launching a bike rental program (primarily) to clear excess inventory.

“If you look at our balance sheet, you’ll see that the business is not going away, which for a long time was a systemic threat. So, because of that, we’re able to focus on renewed growth … I think you’re going to see significant product innovation in the next two years, which I’m very excited about because we have a real shot at changing the growth trajectory of the business.”

- McCarthy, Q2 2024.

Overview and Business Model

Peloton closed 2024 with 6.4 million members spread across 3.6 million paid subscriptions, including 2.98 million Connected Fitness (CF) and 615,000 digital app subscriptions. A “member” is defined as anyone with access to a paid account who completed at least one workout in the past year. Notably, around 10% of CF subscribers own more than one Peloton product—a clear sign of the brand’s appeal.

While Peloton is making moves into commercial spaces like hotels and campus gyms (we’ll touch on that later), over 90% of its CF subscriptions are held by households. Members are highly engaged, averaging 14 workouts per month per CF subscription in 2024.

Peloton currently operates in five key markets, with the U.S. accounting for about 90% of its revenue, followed by the U.K., Canada, Germany, and Australia. Its distribution strategy combines direct sales with third-party (3P) retail and logistics channels. However, in Austria (and soon Germany), it relies exclusively on 3P partners.

Roughly two-thirds of Peloton’s lifetime sales have come from hardware, with bikes making up about 90% of the units sold. Beyond its flagship products, Peloton offers the Guide, a personal training device, as well as a range of accessories and apparel.

Hardware

Peloton’s hardware pricing, including delivery and setup, ranges from $1,445 to $2,495 for the Bike and Bike+, $2,995 for the Tread, $3,295 for the Row, and $6,000 for the Tread+. The pricing is competitive within their category tiers, though Peloton offers fewer models compared to rivals like NordicTrack, which has eight treadmills to Peloton’s two, and Hydrow, which offers three rowers to Peloton’s one.

To paint with broad strokes, Peloton’s hardware stands out with its sleek, minimalist design, whisper-quiet operation, and premium materials like soft-touch coatings and carbon steel—while many competitors rely on lower-grade plastics and standard finishes.

Peloton also excels with its industry-leading software and user-friendly interface, but it’s the content that drives its high Net Promoter Scores (NPS) and fosters deep customer loyalty.

The Tread+ is not currently available outside of the U.S., and the Row is only available in Canada outside its home market.

Content

Peloton streams over 1,000 live classes each month, across 16 modalities in English, German, and Spanish. Its cutting-edge studios in Hudson Yards, NYC, and Covent Garden, London—both located in prime, affluent areas—offer distinct advantages despite their significant costs.

The cycling studios are the largest, with 39 bikes in NYC and 24 in London. Nestled in two of the world’s most visited cities, they’ve become pilgrimage sites for many Peloton members when traveling. Classes, priced at around $35 per session, fill up very quickly.

This intense demand highlights members’ enthusiasm, especially when they have the chance to meet their favorite instructor—a moment that often leaves them starstruck. It’s more than just fan service; it’s a well-oiled loyalty engine that reinforces Peloton’s unique place in the fitness world.

Unsurprisingly, the energy in these classes is palpable, even for those tuning in remotely. Features like Peloton’s leaderboard and social tools—like high-fiving fellow riders—amplify the sense of community. But what truly sets Peloton apart is its seamless integration of music, powered by the company’s proprietary platform.

Music, as it turns out, is no small matter. Delivering this perfectly synchronized experience requires securing public performance, reproduction, and synchronization rights—unlike radio stations, which only require performance rights. The result? A finely tuned experience where, when an instructor calls out “Right, right,” your foot instinctively follows the beat, pulling you deeper into the workout. In 2024, Peloton spent $137 million on music royalties, accounting for 25% of its subscription cost of revenue.

Instructors, with the help of music experts, curate playlists for each class, and members often choose sessions based on the music selection. In contrast, many other platforms rely on unsynchronized background tracks—if they even offer music at all—and typically have limited in-studio class sizes, if any. To fully grasp these advantages, take a look at these clips comparing Peloton with its main rival, iFIT, where the differences are striking.

In recent years, Peloton has leaned heavily into non-cycling content, particularly strength training—the most popular form of at-home exercise in the U.S.

Peloton’s focus on high production value, diverse content, and expanding entertainment options1 has resulted in a 75% increase in monthly workouts per CF subscription since 2018.

Subscriptions

Peloton offers three subscription tiers: the All-Access Membership for hardware users at $44 per month, and two digital options—App One at $13 and App+ at $24. The key difference between the digital tiers is that App One limits access to equipment-based classes, while App+ offers unlimited access to all classes, including performance metrics. The company also partners with employers, insurers, and other enterprise clients to subsidize access to both the Peloton App and All-Access Membership for employees and members.

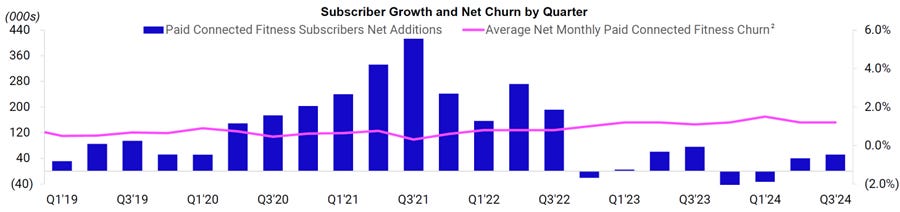

Retention

In 2024, the average net monthly churn rate for CF subscriptions was 1.4%, compared to approximately 5% for rentals and 7.7% for paid app subscriptions. The CF churn rate has risen above the five-year average, primarily due to a revenue shift toward higher-churn segments, particularly secondary market subscribers.

Secondary market subscribers show slightly higher churn rates than those acquired directly. As this segment has grown, so has overall CF churn. In response, Peloton has introduced new initiatives aimed at improving the buying and onboarding experience for these users.2

Higher churn has also been observed among cohorts acquired after the initial COVID boom, when Peloton started aggressively targeting non-core demographics, particularly Gen Y and Gen Z—a strategy now seen internally as a misstep and subsequently scaled back.

Competitive Landscape

Peloton faces competition from fitness apps, mid-tier and higher-end gyms, boutique fitness studios, and other connected fitness providers. Recall iFIT, its main rival and the parent company of brands like NordicTrack, ProForm, Weider, and Freemotion, which has long been a key player in the industry.

iFIT offers a broader range of equipment, from entry-level to premium, and maintains a stronger foothold in the commercial market, while Peloton has remained primarily consumer-focused. The sharpest divergence, however, is in their subscription businesses—where iFIT has faltered despite the bold projections in its since-withdrawn 2021 S-1 filing.

At the time, iFIT’s engagement was half of Peloton’s, with a churn rate more than double. Yet, iFIT touted its connected fitness platform as “unmatched” and predicted significant market share growth. The reality has been quite different: since March 2021, Peloton has added approximately one million net connected fitness subscriptions and doubled its revenue, while iFIT has lost around 500,000 subscriptions. This pattern extends to other competitors like Bowflex and Echelon.3 Despite steady hardware sales, neither has cracked the subscription model.

Barry McCarthy understood early on that success in hardware was secondary to winning in content and shifted Peloton’s focus accordingly. As he put it in May 2023:

“So, do I want to sell hardware? Or do I want people engaged in the content? I want people engaged in the content. If you want to consume it on our platform, that’ll be a terrific experience. But if you bought somebody else’s hardware, we’d still be delighted to have you.” He added, “If you can afford a Mercedes, great—we’ll take a Mercedes. But if all you can afford is a Ford, then we'd be delighted to sell you a piece of the Magic Kingdom.”

And Peloton has indeed sold thousands of those “pieces of the Magic Kingdom” to users of competitor hardware. Indeed, there’s even a Facebook group called “Peloton Digital App users + Echelon Bike Riders” with over 11,000 members.

What’s Next for Connected Fitness?

Peloton wasn’t the only company to overextend during the pandemic-fueled home fitness boom. Capital flowed into connected fitness like the next gold rush, but the surge was followed by an inevitable correction. Since 2019, Peloton’s main competitors—iFIT, Hydrow, Echelon, and Tonal—raised over $1.5 billion collectively. Yet, as the dust settled, the sector found itself grappling with financial instability and rounds of layoffs. Bowflex, for instance, filed for bankruptcy in May 2024.

With capital drying up, these competitors are likely to lose ground as the industry consolidates. As rivals tighten their belts and cut spending—particularly on high-cost advertising targeting Peloton’s core demographics—Peloton stands to benefit. Less competition for premium ad placements means lower CPMs, making it easier and cheaper for Peloton to reach its most lucrative prospects.

Additionally, it seems inevitable that competitors will pivot toward more open ecosystems—a trend already in motion—allowing seamless integration with third-party apps like Peloton. This shift will be crucial for driving hardware sales, which remain the backbone of their revenue.

Digital App

Peloton’s real competition on the digital side comes from tech giants like Apple (Fitness+) and Google (Fitbit), but as we've seen in streaming, deep pockets don't always guarantee success—just look at Apple TV and Amazon Prime next to Netflix. Apple has been producing fitness content for years, and while it’s decent, it’s not in the same league as Peloton’s. The same holds true for Fitbit. As one former Peloton VP of Content Production bluntly put it: “I know what Apple spends on their content. I know what Peloton spends on theirs. It’s clear which one is really making it.”

Peloton’s content engine, fueled by millions of engaged members, has created a virtuous cycle: top talent flocks to the platform, eager to build their personal brands and land licensing deals. But as Apple Fitness demonstrates, it’s not just about audience size—it’s about the power of the Peloton brand and the doors it opens.

Of course, this begs the question: what happens if Peloton’s star instructors jump ship to Apple Fitness or another competitor? The so-called “instructor exodus,” where three instructors left amid contract talks, did raise eyebrows. But with 59 world-class instructors on board, losing a few is hardly a crisis. Peloton’s connected model, where members invest in expensive equipment and belong to a tight-knit community, adds a protective buffer. When one instructor exited and criticized Peloton, it quickly became clear where members’ loyalties lay—and the content disappeared from the platform.

These dynamics explain Peloton’s dominance in app store rankings and its digital growth potential. But this confidence wasn’t always there. Before its 2023 relaunch, the app wasn’t exactly making waves. Leaked communications from January 2022 revealed one executive’s blunt take: “Our app is terrible.”

Still, Peloton’s app suffers from low awareness—just 6%, compared to over 55% for the Bike. That disparity signals a huge growth opportunity. As McCarthy noted in Q2, “The app is the best product we have that nobody knows about.”

Community

While Peloton’s missteps and controversies have certainly left a mark—though often overstated—it has achieved something few others have: building and sustaining a fiercely loyal, engaged community. This is evident in the presence of at least three podcasts solely dedicated to Peloton, each consistently producing content for several years.

It’s no surprise that Peloton was featured on the popular podcast Sounds Like A Cult in 2023. The hosts, while making playful comparisons to actual cults, noted: “… [Peloton] doesn’t require you to recruit anyone, but you just want to … Once you get hooked, you’re going to want to evangelize it to all your friends … you want them to join because it’s something that changed your life for the better…”

A powerful example of this community spirit was on full display when Peloton Tread instructor Susie Chan participated in the Badwater 135 Ultramarathon, considered the world’s toughest race. A group of Peloton members, known as "Susie’s Striders," organized a relay challenge to support her, ensuring that at least one member was running—on their Tread or outdoors—for the entire 41-plus hours it took her to finish the race. Some even woke up at 2 or 3 a.m. to make it happen.

Few brands have cultivated such dedicated communities around them.

Member Profile and Value Proposition

So, who is Peloton for? Primarily, it’s for people who want to stay fit without the hassle of going to the gym. While some users might still frequent a gym or boutique fitness studio, they’re likely in the minority. Peloton’s core demographic skews toward middle-aged, upper-middle-class or higher-income households—people less concerned with subscription costs and more interested in avoiding the typical gym scene, especially the younger, more boisterous crowd (no offense, gym bros!).

The membership also leans heavily female, a group generally more drawn to group fitness classes.

For many, owning a Peloton marks the first time they’ve maintained a consistent fitness routine. The reasons are clear: convenience, privacy, top-tier instructors, and the commitment that comes with a sizable financial investment. At the core of Peloton’s value proposition is convenience—eliminating the hassle of commuting to the gym, especially during winter or when juggling kids, a demanding job, or both.

Then there’s the economics. Members view Peloton as a long-term investment, and when spread over several years, the cost often compares favorably to popular alternatives. High-end gym memberships, like Equinox, typically range from $70 to $150+ per month. Boutique fitness classes can run $20 to $40+ per session, and personal trainers command $50 to $150+ per hour. While Peloton isn’t a direct substitute for these, it offers a highly practical, cost-effective alternative—and, at its price point, arguably the best option available.

Financial Snapshot and Unit Economics

Peloton’s revenue peaked in 2021 at $4.02 billion, driven by $3.15 billion (78%) from hardware sales. In 2022, operating losses reached a whopping $2.73 billion. Since then, the company’s revenue mix has shifted, with subscriptions overtaking hardware sales for the first time in 2023. Gross margins for these segments have moved in opposite directions.

Restructuring efforts have primarily targeted COGS, alongside significant cuts in S&M and G&A (see 2024 vs. 2022). Peloton expects to wrap up the remainder of its ~$200 million restructuring plan this quarter, which includes ~$100 million in headcount reductions and ~$50 million in S&M cuts.

In May 2024, Peloton completed a major refinancing, securing a $1 billion five-year term loan and $350 million in oversubscribed convertible senior notes due 2029, with interest rates of 12.4% and 5.5%, respectively. Proceeds from the notes and new credit facilities, along with cash on hand, were used to repurchase $800 million of 0% convertible senior notes due in 2026 at a discount (~$200 million remains outstanding) and refinance its term loan and revolving credit facilities.

As expected, Peloton’s financial struggles have led to a hefty accumulation of NOLs, totaling $3.3 billion at the federal level and $2.6 billion at the state level.

In 2024, hardware gross margins improved notably, with Peloton now targeting low double-digit margins, according to CFO Liz Coddington. This is expected to be driven by reduced promotions, supply chain efficiencies, and a more favorable revenue mix, especially with a stronger focus on Treads. The company also doesn’t expect the inventory write-offs that weighed it down in the past.

Peloton turned Adjusted EBITDA positive for the first time in three years and posted positive FCF in the last two quarters. While encouraging, stock-based compensation expense (SBCE) remains a drag, still well above the five-year per-employee average.

Looking ahead, SBCE is likely to align more closely with the annualized value of USBC, barring any significant workforce expansion.

It’s worth noting that Peloton could reduce its marketing from 25% of sales to 10% and its R&D from 11% to 5%, and it would still outspend the next highest competitor, according to BMO. While such drastic cuts are unlikely, the key takeaway is that Peloton has plenty of room to scale back spending without jeopardizing its market position.

LTV to CAC

Like all subscription-based businesses, Peloton’s success hinges on its LTV to CAC ratio (Lifetime Value to Customer Acquisition Cost). Peloton defines LTV as the present value of the expected gross profit generated by a customer. While the company aims for a 2-3x ratio, it has hovered around 1 to 1.5x in recent years.

Peloton’s unit economics are less favorable for rentals than for equipment sales, due in part to more demanding working capital requirements. However, the rental program has demonstrated strong incremental value, with over 60% of subscribers stating they wouldn’t have signed up without it. Rental economics are more favorable for higher-priced hardware, especially when buyout rates increase and refurbished inventory is used (primarily from 30-day trial returns).

Total Addressable Market (TAM)

Before we dive into Peloton’s growth prospects, let’s quantify the opportunity. Global health and wellness spending surged to $5.6 trillion in 2022, up from $4.2 trillion in 2017, according to the Global Wellness Institute (GWI). That figure is projected to reach $8.5 trillion by 2027, with the physical activity sector growing at around a 7% compound annual rate.

The pandemic, unsurprisingly, accelerated health awareness way above trend, with fitness app usage soaring 50% above pre-pandemic levels by mid-2020. This heightened focus hasn’t waned—58% of U.S. respondents in a 2024 McKinsey survey said they’re prioritizing wellness more than they did a year ago.

The fitness sector is also booming. U.S. gym memberships hit an all-time high of 69 million in 2022, up from 64.2 million in 2019. Meanwhile, over 30% of Americans now use health-tracking devices, and Amazon saw a 25-55% spike in sales of supplements and alcohol-free beverages in 2023.4 In short, the health and wellness sector isn’t just growing—it’s thriving.

Peloton estimated that over five million treadmills and nearly three million stationary bikes were purchased for home use across its core markets in the year ending March 2019. As expected, most of these sales came from entry- and mid-level price points. For example, Jungle Scout data shows that in the three months ending July 2024, sales of treadmills priced between $1,000 and $2,000 on Amazon were more than four times higher than those above $2,000. This is why, after introducing the smaller Tread (priced at $3,000, half the cost of the Tread+), management saw the treadmill category as a 2-3x opportunity compared to the bike.

As mentioned earlier, Peloton’s unaided brand awareness lags significantly in international markets—37% in the U.K. and somewhere in the 20s in Germany. The awareness gap between Peloton’s bike and non-bike products is likely just as wide abroad as it is in the U.S., leaving ample room for growth across both product lines and geographies.

However, the digital app (soon to be “apps”) could be the real linchpin for Peloton’s expansion. It offers an asset-light way to deepen market penetration and reach new regions, while efficiently drawing more users into Peloton’s ecosystem. Customers who start with the app are far more likely to choose Peloton hardware when they’re ready to upgrade or make their first purchase, making it a powerful conversion tool.

“You’re going to be surprised how much TAM was unlocked by the digital app,” McCarthy said in 2023.

The Next Chapter: Growth and Improvement Opportunities

“It’s pretty clear that innovation drives growth. We’ve been busy saving ourselves the last two years but now we’re positioned to invest in innovation. Again, it’s innovation that put us on the map in the first place. There’s a lot of talent in the building. It’s a matter of getting it organized and focused in a really productive way.”

– McCarthy, Q2 2024

If this analysis was helpful, a thumbs-up would mean a lot. Have thoughts or questions? Drop them below!

Leadership and Company Culture

While McCarthy’s leadership tackled many of Peloton’s cultural challenges, some issues lingered. A former VP of Content Production, who left in July 2023 after two years at the company, shared his perspective: “He was very direct. To me, he was saying the right things, but the message wasn’t landing. It was like he was speaking English to a Spanish-speaking company.

“When he said, ‘We don’t have enough money. We’ve got to become cash flow positive ASAP,’ I took him at his word and started making changes—even more than most. But my colleagues didn’t budge. I can’t tell you how many times a manager said, ‘I don’t want to do that. I just don’t want to.’”

Peloton also struggled with silos, where teams worked in isolation, leading to minimal collaboration across divisions. R&D, for instance, developed features without consulting other departments, sometimes resulting in costly redundancies. A lack of accountability compounded these problems.

However, the former VP noted the recent restructuring might have addressed this: “Anecdotally, the people let go from my group were the ones not pulling in the same direction. They had been protected until now, which was my frustration, but they’re gone. This could be Peloton’s chance to start fresh.”

With a new CEO on the horizon, there’s optimism that the company can finally root out any remaining cultural issues and reset for good.

R&D Reboot

Nick Caldwell, who took over as Peloton's Chief Product Officer in November 2023, replacing co-founder Tom Cortese, appears to be the change agent the company’s product and R&D teams have been waiting for.

Caldwell’s track record underscores his ability to move fast and deliver results. At Twitter, he led nearly 2,000 engineers and orchestrated a lightning-fast overhaul of the Explore page in just three months. Earlier in his career at Microsoft, frustrated by the slow pace of product rollouts, Caldwell famously thought, “I could do this way faster,” and proved it by rallying a team to launch the first version of Power BI—demonstrating his knack for swift execution, even in uncharted territory.

Caldwell’s “superpower,” as some call it, lies in managing teams and setting clear product roadmaps—skills honed over 15 years at Microsoft, a company he credits with having a “massively underrated approach to organizational design.” While he pushes his teams hard, he’s known for inspiring loyalty. As one former colleague put it, “When Nick moved from Seattle to San Francisco, several people packed up their homes and families to work with him again.”

With tech debt resolved and organizational issues largely addressed, we expect a much faster pace of innovation under Caldwell’s leadership.

Marketing Transformation

“There’s a feeling inside the company that we haven’t done a great job of helping potential users understand what our existing members already know,” McCarthy admitted in 2023. David Rosenthal, co-host of the popular Acquired podcast and part of Peloton’s target demographic (household), offers a telling example:

“I had been hearing from plenty of my friends how much they love [Peloton] for years, and that wasn’t even enough to put me over the edge … Then we went on vacation before our daughter was born and the hotel had a Peloton bike. [Trying it] I was like, oh, this is awesome, and my $200 Amazon bike in the garage—it’s night and day compared to this.”

We can say from personal experience that Rosenthal’s story is more the rule than the exception. That’s why expanding Peloton’s commercial footprint is crucial, as hotels and universities provide a low-pressure way for potential customers to try the product firsthand. But that’s only part of the solution—more targeted messaging is also key to closing the gap.

In January 2024, Lauren Weinberg joined Peloton as CMO. Known for her passion for analytics, Weinberg isn’t your typical marketing executive. “A lot of CMOs don’t want to get into the weeds, but I love it. I’m definitely a little nerdy that way,” she admitted.

Weinberg’s career gained momentum at Yahoo, where she wasn’t afraid to challenge the status quo. “I told the CMO, ‘Yahoo’s marketing could be so much better,’” she said. Her push for a data-driven approach worked, but the resistance to change eventually wore her down.

Her next role as CMO at Square (now Block) marked a turning point. When she arrived, Square’s messaging was purely functional—“it’s easy, it’s free, it’s fast”—but Weinberg saw the need for emotional resonance. She overhauled the company’s marketing, blending data-driven targeting with brand-building. “There was no one we wanted more than Lauren for that role, so we got very lucky,” a former senior executive remarked.

Weinberg encourages her team to “speak up, ask hard questions, and challenge the way we’ve always done things.” Her bold, data-led approach seems to be exactly what Peloton needs.

Hardware and Product Innovations

V3 Bike

Before we dive into what’s next for the Bike, let’s briefly compare it to the Bike+ (released in 2020).

The Bike+ features a larger 23.8-inch screen with a full 360-degree swivel, a clear upgrade over the fixed display of the original. It also runs on a faster, more responsive interface, thanks to a beefed-up processor and extra memory. The Auto-Follow resistance system, which automatically adjusts to instructor cues, stands out as a key improvement over the manual setup of the original. Add to that a better sound system and a sleeker design, and the Bike+ is clearly the more modern machine.

What’s Next

The next iteration of the Bike promises more than just a few cosmetic tweaks. Recent patent filings offer a sneak peek at what’s coming:

US20240183484A1: Display Mounting Systems and Methods As the title suggests, this patent focuses on display mounting systems, but it also reveals a noteworthy addition: a four-microphone array for advanced voice control. The current models do not have microphones.

US20240198204A1: Actionable Voice Commands Within a Connected Fitness Platform outlines a key use case for the microphones—a virtual assistant that enables hands-free interaction during workouts.

US20240226662A1: Handle Control Systems and Methods for Exercise Equipment describes hands-free resistance adjustment mechanisms, which could either replace or complement the traditional resistance knob.

The addition of microphones could introduce real-time, mid-ride communication, adding a social element currently missing from the market. This fits with Peloton’s focus on community features, like private teams, which saw over 20,000 created in just two weeks.

While it’s hard to say how game-changing these hardware updates will be—some might be just nice-to-haves—they offer a solid opportunity to drive replacement demand and attract new customers, potentially boosting both volume and market share. Plus, who knows what other Bike updates could be in the pipeline.

Meanwhile, Peloton’s “Zwift-style” game, set to launch in beta, could be another major catalyst for engagement and sales. The feature will allow users to “cycle in a virtual training environment, with a personalized avatar riding through simulated landscapes, either solo or with other virtual riders.”

For those unfamiliar, Zwift is a hit in the cycling world with over a million subscribers, but it’s never been practical for non-cyclists. While it’s unclear how closely Peloton’s version will mirror Zwift, it’s the first mass-market alternative designed for everyone. If it’s even halfway decent, it could make a big impact—at the very least, it might reignite engagement for users like me who don’t interact much with the classes.

“Win Tread”

In 2023, McCarthy highlighted the much-anticipated return of the Tread+, which had been off the market for nearly two years: “The one product at Peloton that you couldn’t pry out of a member’s dead hands is the Tread+. They are fanatically obsessed with the user experience… but we’ve never been able to sell it.”

Obsessed indeed. The Tread+ relaunch in Q3 led to a 42% surge in treadmill revenue in Q4 Y/Y, with CNN naming it the best treadmill of 2024. Meanwhile, the smaller, more affordable Tread holds its own, boasting an impressive 73 NPS score. New software features—one praised as Peloton’s “best in years”—have further sharpened the product lineup.

Still, Peloton’s brand awareness in the treadmill market remains surprisingly low. Hence the enthusiasm of the interim co-CEO last quarter: “Tread remains an incredible, underdeveloped opportunity for Peloton—one of our highest potential growth levers.”

While these factors explain management’s bullish outlook, there’s likely more in play. As hinted earlier, Peloton’s recent patent application could be its secret weapon. The potential is easy to grasp—just look at the buzz surrounding a competitor’s product set for release this fall.

The holy grail for treadmill makers—technology that adjusts pace based on user movement—has been elusive, stymied by technical and liability challenges. Enter Wahoo’s KICKR RUN, a $5,000 machine hailed as a “gamechanger for indoor running” and “the best treadmill ever made.” Its ToF (time-of-flight) sensor tracks a runner’s position 1,000 times per second, automatically adjusting speed. Move forward, it speeds up; drift back, it slows down—no buttons required.

“Anyone who has run on it wants to buy it immediately,” said Wahoo co-founder Chip Hawkins. But words only go so far. For a real sense of the excitement, just listen to tech reviewer DC Rainmaker:

So how does Peloton stack up? Unlike Wahoo’s single-sensor system, Peloton uses multiple ToF sensors paired with advanced safety features. Its setup divides the treadmill into zones—front, center, and rear—tracking user movement in real time while monitoring leg motion. It also alerts users if they drift too far or show signs of fatigue, and adjusts accordingly if abnormal movement or a fall is detected.

Interestingly, Wahoo hasn’t patented its technology, nor has it hinted at any pending applications. Perhaps it’s within the non-disclosure window—or maybe they didn’t file, doubting the tech would pass novelty or non-obviousness tests. That’s a gamble in a crowded field of automatic treadmill speed control patent applications.5 Still, the only serious competitor to Peloton’s patent seems to be the University of Nebraska-Lincoln (UNL).

UNL’s patent application also uses multiple ToF sensors but with notable differences.6 The timing is particularly intriguing: UNL filed its provisional patent just six weeks after Peloton in May 2021, and both full applications were published in July 2024. Under the U.S. first-to-file system, Peloton has the advantage—assuming there’s no prior art from UNL, which seems unlikely based on public information (and the veil of secrecy around such projects).

The fact that both applications are still active after more than two years is promising. If the USPTO had serious concerns about novelty or non-obviousness, they likely would have shut them down by now. Either way, Peloton seems set to bring this technology to market—with or without a patent. And it will almost certainly make its way into the more affordable Tread, given the minimal incremental cost.7

This kind of innovation could significantly reduce price sensitivity. It’s the type of feature that turns a great product into one that “creates an anxiety only relievable by purchase,” as marketers like to say. Consumers satisfied with a $1,000 to $2,000 treadmill might suddenly find themselves willing to pay more.

Lastly, Peloton is pursuing commercial certification for the Tread+, particularly exciting given its recent partnership with Hyatt (more details to follow).

Doubling Down on Running

Peloton is making moves into outdoor fitness with its acquisition of technology from Ghost Pacer, a startup specializing in AR tech for runners. Ghost Pacer gained traction in 2020 when its Kickstarter campaign hit its funding goal in under an hour, eventually raising over $150,000 from more than 800 backers. The AR glasses were initially priced at $349.

Now, with two patent applications (US20240264264A1, US20240151981A1) in hand, Peloton looks poised to expand its footprint in the running and outdoor fitness space. Wearable AR technology could help the company reach a wider fitness audience, appealing to everyone from dedicated runners to those wanting to mix up their indoor routines.

Digital and App Initiatives

Peloton is also targeting gym-goers with the beta launch of “Peloton Strength+,” a standalone app designed to deepen engagement with members and attract new subscribers. The goal? To become “core to the gym.”

“There’s a huge community, myself included, of people who prefer training at the gym, and we want to break into that market,” said Peloton instructor Andy Speer. With nearly 69 million gym members in the U.S.—many of whom align with Peloton’s target demographic—the opportunity is significant.

“The custom workout builder let me specify my desired workout duration, target muscle group, difficulty level, and equipment access. I was served up a one-off gym plan based on my settings, with the option to swap out moves one-by-one or entirely refresh my curation until satisfied with the routine. As someone with a knee that needs low-impact training, I definitely appreciated the option to replace squat jumps with weighted squats. Programs are a bit more tailored, with gym plans created and the involved moves demoed by Peloton instructors, complete with the kind of audio guidance you might get from an actual personal trainer moving around the machines alongside you.”

- Kate Kozuch, Tom’s Guide

Personalization

“The better we are at personalization, the more engaging the user experience, the stickier it becomes, the lower the churn, the happier the members—and the more organic growth we’ll see. That’s the playbook for success,” McCarthy said.

Drawing on his experience at Spotify and Netflix, McCarthy made personalization a key investment priority at Peloton. The company has made notable progress, especially in content discovery, making it easier for members to find and engage with the right workouts.

Recently, Peloton introduced personalized plans tailored to specific fitness goals, such as building strength or losing weight. These plans combine personal training expertise with machine learning to generate weekly class schedules suited to each user’s needs.

This feature addresses a common challenge: many people don’t know how to design a fitness plan aligned with their goals—or simply don’t want the hassle. Peloton’s new feature removes that friction, making the experience seamless for its users.

Commercial and Corporate Partnerships

Peloton for Business is quickly becoming a major growth driver, with the potential to boost both app subscriptions and hardware sales. One of the most exciting partnerships to date is with Hyatt, signed earlier this year. This collaboration will outfit over 800 Hyatt properties with Peloton equipment and, for the first time, give guests access to Peloton classes on in-room TVs at nearly 400 locations. Hyatt is also the first hospitality brand to link its rewards program with Peloton, allowing guests to earn World of Hyatt points for working out—redeemable for future stays, upgrades, or experiences.

This builds on Peloton’s established partnership with Hilton, which has already placed Peloton Bikes in over 5,400 Hilton-branded hotels worldwide. According to Hilton, 98% of survey respondents prioritize wellness activities while traveling, a figure that aligns perfectly with Peloton’s offerings. In fact, 90% of Peloton Members say they’re more likely to stay at hotels with Peloton equipment.

Up until now, hotel partnerships have featured only Bikes. The Hyatt deal, however, marks the first to include the Peloton Row, which gained commercial certification in October 2023, and presumably the Tread+ once certified. Former president William Lynch noted that each Peloton Bike in a hotel led to seven sales.

With the Row and eventually the Tread+ expanding into both new and existing hotel partnerships, these products will gain significant exposure to millions of guests within Peloton’s core demographic. In the year ending November 2023, over 7.5 million rides were taken on Peloton bikes in commercial settings—a figure that’s set to rise as more hotels join the roster and introduce the Row and Tread+.

In addition to hotel partnerships, Peloton offers enterprise partners discounted hardware and subscriptions for employees. While this segment is small, it shows strong promise, boasting a renewal rate of 93% as of September 2023. For example, law firm O’Melveny & Myers LLP saw 42% of eligible employees enroll in Peloton’s Corporate Wellness program within a year, far exceeding typical engagement rates of 3-10%. “We’ve got something special here,” said the firm’s Benefits and Well-Being Manager, Monica Rocha.

As Peloton continues to innovate its hardware and digital offerings, expect higher renewal rates, deeper engagement, and more conversions through commercial and corporate partnerships.

Google Partnership

Last month, Peloton and Google announced a partnership granting Fitbit Premium members access to Peloton’s suite of classes at no additional cost. Soon, the Fitbit app will expand to feature a broader catalog of Peloton content, while free users will get access to a limited selection. Of course, Fitbit benefits by offering its subscribers superior content, while Peloton stands to gain from exposure to Fitbit’s roughly 40 million monthly active users, tapping into a larger, health-conscious audience.

Valuation

Peloton projects adjusted EBITDA of $200 to $250 million for 2025, alongside at least $75 million in FCF and a 50% gross margin. As CFO Liz Coddington emphasized yesterday, “I want to be clear that we are not factoring in any upside” from potential subscriber growth or reduced churn tied to the recent initiatives. The guidance also accounts for a somewhat softer macroeconomic outlook.

The model below represents our base case, incorporating a layer of conservatism based on the factors we’ve discussed. I’ll outline the bull and bear scenarios below.

Notes and Assumptions

Digital AMR and hardware ASPs: These are rough estimates, both historically and projected.

Churn: We expect a 10-basis-point decline in 2025, with further improvements throughout the forecast period. This strikes me as a cautious estimate, considering the significant potential gains from advancements in gamification and personalization.

Subscriber growth: Anticipate a notable uptick driven by the innovation pipeline and aided by reduced churn. This assumes a stable, if not slightly softer, economic backdrop—a prudent baseline, not a bold prediction.

Price hike: Likely to occur in 2027/2028.

Working capital: Expected to grow incrementally, driven largely by increased hardware sales (ramping in 2026 and 2027).

International expansion: Anticipated to deepen penetration in existing markets and expand into new ones, with a stronger focus on asset-light third-party models and notable digital growth.

Debt: We estimate Peloton will reduce its term loan by around $125 million in 2025, bringing the net balance to $825 million, followed by further repayments of roughly $75 million in 2026 and $150 million in 2027, along with settling the $200 million in convertible notes due in 2026.

Cash: Projected to end at approximately $600 million in 2025, $500 million in 2026, and $600 million in 2027. These figures are lower than historical levels, reflecting more efficient use of cash reserves. CFO Liz Coddington has noted that Peloton currently holds more cash than is needed for its operations.

Enterprise Value: Assumes no major lease renewals, with around 17 million shares of dilution per year through 2027—though this figure could fluctuate depending on various factors.

Based on the current stock price and implied expectations, a scenario like the one outlined above would justify a share price north of $10—potentially much higher. Applying the current consensus EV/EBITDA multiple of 13.6x to our 2026 forecast suggests a share price in the $12 range, climbing closer to $15 by 2027.

Bull and Bear Scenarios

Bull case: If Peloton can drum up even moderate excitement around its upcoming hardware rollouts, hitting 3.5 to 4+ million Connected Fitness subscribers over the forecast period is within reach—especially if churn declines slightly. The digital and app initiatives have real potential to boost both subscriber growth and engagement.

Bear: The model starts to crumble without at least modest growth or a stable subscriber base. A drop of 100,000 to 300,000+ CF subscribers, without recovery by 2026-2027, would put Peloton in a difficult position. If the digital app doesn’t offset the decline—a long shot if CF subs drop that much—Peloton could face serious trouble.

Acquisition Target

Speculation about Peloton as an acquisition target has been swirling for years, with frequent rumors pointing to tech giants like Apple or Google. Deepwater Asset Management even predicted that Apple could make a move in 2024. The investment logic is clear—either company could seamlessly integrate Peloton’s premium content library into every iPhone or Pixel, along with significant synergies.

However, the current political climate isn’t exactly rolling out the welcome mat for such deals. Competitors would undoubtedly raise strong objections, arguing that granting Peloton virtually unlimited resources would stifle competition. While consumers might see short-term benefits through faster innovation, better device integration, or lower prices, the risk of long-term monopolistic pricing would loom large.

Private equity? It’s tricky to predict, but the odds must improve if Peloton’s growth trajectory becomes clearer and shows potential for substantial gains.

Risks

A key risk to the thesis lies in the rollout of Peloton’s Tread technology. While the current Tread+ is an excellent product, we believe it has met its match in Wahoo’s KICKR RUN. If Wahoo’s launch goes smoothly and Peloton doesn’t quickly counter with its own tech advancements, our outlook for the category will become considerably less optimistic. Granted, Wahoo’s first-gen products haven’t been flawless, and its shorter warranty (one to two years versus Peloton’s three to six) remains a weak spot. But relying on warranty coverage to fend off innovation is shaky ground.

After more than three years of development and a hefty R&D investment backed by top engineers, Peloton’s tech should be ready—or close to it. It’s possible the company is timing its release with the next generation of the Bike or Row—the latter also receiving upgrades. But there’s still the chance that development hurdles persist. If delays stretch beyond 18 months, our outlook will turn more negative—much like it would for the Bike, though to a lesser extent.

Other risks:

The innovation pipeline fails to drive meaningful demand, either in hardware or elsewhere.

Efforts to boost engagement and reduce churn underdeliver.

Rising competitive pressure from tech giants like Apple or Google in the app space.

A prolonged deterioration in macroeconomic conditions.

Should any or all of these risks materialize, the impact on Peloton’s financial health and long-term viability could be substantial.

Conclusion

“One of the learnings at Netflix was that you win by having lots of dials to turn to fine-tune the business. You can never be sure which dial will drive performance, but you're only in trouble when you run out of dials. So as long as you’re clear on strategic priorities and resource allocation, having enough irons in the fire ensures you can deliver, even amid uncertainty.”

- Barry McCarthy, May 2023

By McCarthy’s own metaphor, Peloton now has more dials to turn than at any point in its recent history—perhaps ever. And it’s not just the number of dials; it’s the strong likelihood that several will meaningfully shift the company’s growth trajectory.

Analysts and investors have a habit of extrapolating recent trends into the future, despite living in a world that operates in cycles. In good times, forecasts tend to overshoot into optimism; in bad times, they veer too far into pessimism. This tendency, known as recency bias, leads people to place too much weight on recent events when making forecasts. Peloton may soon remind everyone that nothing moves in a straight line forever.

Disclosure: The author or the accounts managed by the author hold shares in Peloton. This can change without giving a prior notice to the reader. This article is for informational purposes only. We may be wrong in our analysis and encourage all readers to come to their own conclusions.

Peloton has expanded beyond fitness classes to include entertainment options such as Netflix, Disney+, YouTube, and Kindle. The platform also offers the game “Lanebreak,” with more titles in beta testing, and features outdoor and scenic content.

To support secondary market users, Peloton introduced the Peloton History Summary, which offers transparency on a bike’s age, usage, and service history. The company also added a $95 activation fee for used equipment in the U.S. and Canada, covering a virtual custom fitting, a first for Peloton. This includes discounts on accessories like bike shoes and mats. Reviews of custom fittings are positive, with many noting that even small adjustments to handlebar height, saddle position, or cleat alignment significantly improve the riding experience. Peloton is likely to extend this service to all members, potentially boosting revenue and retention.

Echelon, founded in 2017 as a budget-friendly alternative to Peloton, operates in a closed ecosystem via its Echelon Fit subscription service, leaning heavily on wholesale partnerships with giants like Costco and Walmart. Meanwhile, Bowflex, traditionally focused on strength training, introduced its digital platform in 2019 and embraced a more open ecosystem. Its C6 bike, for instance, is marketed for its compatibility with the Peloton app.

Jungle Scout Report, “Amazon Data Download: Health, Fitness, and Supplement Products.”

Several related patent applications differ from Peloton’s, either in terms of technology, intended purpose, or filing dates, and are unlikely to pose significant threats to Peloton’s application. For instance, US20240123280A1 and US20240042269A1 involve broader position-detection technologies like radar, sonar, lidar, or vision-based systems. Other patents, such as US11691047B2 and EP3849675B1, combine visual and force inputs aimed at precise speed adjustments for rehabilitation. Meanwhile, US11185740B2 uses sensors to measure body and leg swing velocity.

UNL’s US20240216761A1 emphasizes pace control based on the center of mass (COM) and individual leg movements (heel strikes), focusing on specific motion analysis. Peloton’s approach, by contrast, centers on maintaining the user’s position within a designated zone, detecting issues like fatigue or poor form. This focus on optimizing position, rather than simply mirroring pace, could support Peloton’s patentability. Additionally, Peloton’s patent covers a broader scope, including adjustments to speed, incline, and user movement across multiple detection zones, beyond the use of ToF sensors.

Adding Peloton’s multi-sensor technology could raise treadmill hardware costs by $180 to $350, primarily due to the inclusion of ToF sensors, processing units, and minor motor upgrades. However, these costs could be partially offset by automation advancements outlined in patent application US20240230476A1. The enhanced testing system could lower labor expenses, reduce errors, and increase throughput. As a former supply chain optimization director noted in November 2023: “I never visited the facilities, but they were very manual. They relied heavily on manpower over automation. Automation was a priority in early 2021 when demand surged, but once demand dropped, the business case faded.”