Peloton: Survival of the Fittest

Peloton: Survival of the Fittest

Patent Filings and Other Moves Wall Street Is Missing

“I once described turnarounds as a full contact sport: intellectually challenging, emotionally draining, physically exhausting, and all-consuming … From where I sit today, that pretty much summarizes my experience these last two years … A lot of blood, sweat, and tears have been shed to make Peloton’s turnaround possible … I’ve done my very best to recruit a truly talented exec team to lead the turnaround. If I have one lasting legacy at Peloton, it will be this: You have a GREAT lead team, and although the stock market hasn’t recognized this yet, it will. It’s simply a matter of time.”

– Former CEO Barry McCarthy, final memo to employees, May 2nd, 2024

Introduction

McCarthy’s words may resonate differently now that Peloton’s stock has bounced post-earnings, but his message still holds. While investor sentiment is slowly improving, it’s far from euphoric. Short interest remains high at around 18%, down only 2% since the latest earnings report. Yes, this analysis is slightly delayed—blame another major project (coming soon in The Globe and Mail)—but if my take is even directionally accurate, the current stock price presents an asymmetric risk-reward opportunity.

During his final earnings call, McCarthy remarked, “If you look at our balance sheet, you’ll see that the business is not going away, which for a long time was a systemic threat. So, because of that, we’re able to focus on renewed growth … I think you’re going to see significant product innovation over the next two years, which I’m very excited about because we have a real shot at changing the growth trajectory of the business.”

Peloton has been relatively quiet on the innovation front in recent years, especially with hardware—but that’s about to change. Historically, the company has kept hardware developments under wraps for competitive reasons, as CFO Liz Coddington recently reminded investors. However, thanks to Peloton’s need to safeguard its intellectual property, we don’t need to wait for the next big reveal to know what’s coming. After many hours poring over patent filings, I’ve uncovered some intriguing details—some obvious, others buried in technical jargon.

Sources suggest the third iteration of Peloton’s iconic bike is nearing release. While the current model has aged gracefully, nearly a decade without significant updates is beginning to show. My research confirms that the V3 Bike is on the horizon and promises more than just minor enhancements.

But the real breakthrough may lie in Peloton’s treadmill lineup—a category where it remains an underdog, having sold ten times more bikes than treadmills. Yet the treadmill market is two to three times larger, and Peloton’s recent patent filings hint at technology that promises to disrupt the status quo. If granted, even with narrower claims, the long-term potential could be massive.

Of course, nothing is certain. Navigating the patent system is notoriously complex, and I’ve done my share of exhaustive (and occasionally mind-numbing) research to evaluate the odds, including a deep dive into related patents and applications. No need to worry—I’ve packed most of that into the footnotes!

On the digital and app side, Peloton’s latest initiatives look promising, especially in personalization, gamification, and the launch of a standalone app. These efforts could drive significant subscriber growth, boost engagement, and lower churn. However, management’s fiscal 2025 guidance doesn’t factor in these potential improvements, and consensus estimates are just as cautious.

Consensus forecasts also project flat revenue for 2026. But even modest success from these non-hardware initiatives gives Peloton a strong chance of beating expectations. And that’s without factoring in the impending, innovation-driven hardware sales cycle, likely to start by F2026.

The narrative that Peloton is approaching market saturation doesn’t hold up under scrutiny. The data tells a different story: unaided brand awareness of Peloton’s products remains surprisingly low, even in mature markets—except for the Bike, which has about 57% awareness in the U.S., but much less internationally. Awareness of Peloton treadmills in the U.S. hovers around 20%, while the app and Row barely register at 6% and 4%, respectively.

Moreover, as we’ll explore in the marketing section, “awareness” rarely equates to deep product familiarity. Consumers routinely overestimate Peloton’s cost and underestimate the quality and variety of its content, as well as the broader user experience—making any talk of market saturation premature.

Peloton estimates that over five million treadmills and bikes are sold annually in the U.S. alone. Predictably, most of these sales occur at lower price points. Yet Peloton’s ever-improving digital offering—with its near-perfect 4.9-star app rating—presents a path to capture more customers who either can’t or won’t purchase its hardware, whether due to budget constraints or a preference for not owning equipment.

My analysis suggests Peloton can drastically reduce its debt over the next three years, with a clear path to positive operating income in F2026 and meaningful gains thereafter. This view is at odds with consensus, so I understand the skepticism—I wouldn’t expect anything less from you, dear readers—but there’s a lot about this company that’s misunderstood, both inside and outside the investment community. As we dive deeper, that’ll become increasingly clear.

Here’s what else we’ll explore:

The company’s growing commercial traction, including key partnerships with Google and Hyatt—the latter particularly intriguing.

McCarthy’s claim that Peloton now has a “GREAT lead team,” why it’s the strongest lineup the company has ever had, and why that matters, especially in marketing and R&D.

The evolving competitive landscape, broader industry trends, and their implications for Peloton.

Why Peloton’s efficiency has room to improve beyond what restructuring efforts and public commentary suggest.

Barry McCarthy, whom we’ll introduce more fully soon, was instrumental in stabilizing Peloton. His blunt, no-nonsense approach was exactly what the company needed in a crisis. However, his style was more pragmatic than visionary—not surprising for a career CFO who was thrust into the CEO seat. Now, Peloton requires a leader who can rally the company around a compelling vision, inspire employees, and excite customers.

It’s hard to miss the symbolism of launching a refreshed version of the bike that put Peloton on the map, just as the company prepares to announce a new CEO and turn the page to a new chapter. That leader could be revealed any day now, as interim co-CEO Karen Boone hinted during the last earnings call: “We’ve been very focused on it. We are far along in the process ... We’ve narrowed it down to some very highly qualified candidates ... I should probably under-promise here, but I believe you’ll be hearing from the new CEO on this call next quarter.”

All figures are in USD, and all years refer to Peloton’s fiscal calendar unless otherwise noted. Some quotes may be lightly edited for clarity and flow.

History

In 2011, John Foley, a seasoned business executive and fitness enthusiast, found himself in a cycling class in Manhattan—ground zero for the boutique fitness craze. Just like in San Francisco, Los Angeles, and Seattle, high-end studios like Orangetheory and Barry’s Bootcamp were springing up everywhere, offering the latest must-have experience for the urban, smoothie-drinking, athleisure-clad crowd.

“… That’s where you want to be if you are an up-and-coming instructor in this burgeoning new category … there are so many great instructors at these places that have cult followings … it’s so hard to get spots in those classes. The instant they become available, you even had to do this in Seattle, I remember, but in New York it’s impossible.”

- David Rosenthal, the Acquired podcast

This experience sparked Foley’s game-changing idea: a connected stationary bike that would bring live studio classes directly into people’s homes. The value was clear—no need to live in a boutique hub like NYC to access top-tier instructors, no more scrambling for class slots, no steep per-ride fees, and—most appealing of all—class sizes that didn’t cap at 50. Unlike SoulCycle, there would always be room for one more.

But big ideas come with big risks, and investors weren’t exactly clamoring to buy in. Undeterred, Foley turned to friends and family, raising $400,000 through $25,000 and $50,000 checks at a $2 million post-money valuation. Capital may have been tight, but talent was easier to come by—Foley successfully convinced four co-founders to join him on the ambitious journey.

The team knew the bike couldn’t just be functional; it had to look good enough to earn a place in living rooms, bedrooms, or even offices—after all, most of the boutique crowd didn’t have home gyms. Over the next 18 months, they poured their efforts into prototyping what they envisioned as “the most beautiful bike ever designed.”

“There were a number of things we quickly realized we could improve on,” said Tom Cortese, Peloton co-founder. “For starters, bikes today are loud and clunky, so we threw out the chain. We replaced it with a belt drive—smooth, super quiet. You can bring it home without bothering anyone. We also got rid of the brake pads—it’s all magnets now, passing around the flywheel. It’s awesome.”

The search for their first instructors kicked off in May 2013, with the following ad:

In the summer of 2013, Peloton launched a Kickstarter campaign, setting the price of its bike at $1,500 and aiming to raise $250,000. They exceeded their goal, raising $307,000 from 297 backers. But the outcome wasn’t quite the home run they had hoped for.

“We launched a website at pelotoncycle.com and did some marketing on Facebook, but it was mostly crickets. We’d sell about five bikes a week,” Foley recalled. It became painfully clear that people needed to see and experience the product in person. That realization led to their first store opening at New Jersey’s Short Hills Mall in November 2013.

The success of that first store spurred them to open more in 2014, hire additional instructors, and run their first commercial. With the network effect kicking in, Peloton generated $10 million in revenue that year and secured its first institutional funding round, led by Tiger Global.

Momentum continued to build. By 2015, sales skyrocketed to $60 million, and in 2016, that number nearly tripled to $170 million. Peloton officially joined the unicorn club in 2017, raising $325 million at a $1.3 billion valuation. Then, in August 2019, Peloton filed its S-1 with the SEC.

When “PTON” debuted on the NASDAQ a month later, it ranked as the third-worst “mega-IPO” since the financial crisis. Still, this wasn’t exactly a flop—Peloton raised $1.16 billion at $29 per share, reaching the upper end of its target range. And then, on March 11, 2020, the World Health Organization declared COVID-19 a global pandemic.

Within six weeks, over 1.1 million people had downloaded Peloton’s app, and Q4 revenue surged 170% Y/Y. Demand for bikes and Treads soared to the point where customers faced months-long waits, and some resold their equipment at hefty markups. Peloton quickly became one of 2020’s standout stay-at-home stocks—a “pandemic darling.”

“COVID was the marketing campaign that Peloton never could have afforded. The growth that happened during COVID propelled the business to scale in a way that no other company has achieved. That afforded access to capital that it wouldn’t otherwise have and made it the dominant player in the connected fitness category.”

– McCarthy, from a December 2022 interview

As vaccines rolled out in late 2020 and gyms began to reopen, questions loomed about Peloton’s post-pandemic future. The stock peaked soon after, but Foley’s confidence never faltered. In February 2021, he boldly predicted, “We will continue to be a high- or hyper-growth company for years and years to come … you have to think about how you make millions of treadmills a year, three or four years from now … but not getting over your skis with fixed costs and overhead.”

Yet Peloton had already done just that. By early 2021, the company had increased manufacturing capacity by over 700% Y/Y, while also pouring money into retail showrooms, warehouses, last-mile delivery fleets, and a workforce that swelled from 2,000 employees in 2019 to over 8,500 in just two years.

“There is but one step between the sublime and the ridiculous,” Napoleon famously remarked during his retreat from Russia in 1812. Peloton’s own retreat from its pandemic highs echoes that sentiment. The cost of these largely self-inflicted missteps—restructuring, impairments, recalls, and litigation—topped $2 billion. Under increasing shareholder pressure, CEO John Foley stepped down in February 2022.

Enter Barry McCarthy, a no-nonsense operator with a sharp, analytical mind, best known for steering Netflix and Spotify through periods of rapid growth as CFO. As CNBC’s Gabrielle Fonrouge put it, “employees breathed a sigh of relief to have what felt like an adult in the room, someone who’d be able to clean up a multibillion-dollar mess.”

McCarthy summed up Peloton’s leadership failures by contrasting them with his former colleagues. “What makes Reed Hastings and Daniel Ek such great executives is that they deal with the world as it is, not as they want it to be … The Peloton team didn’t exhibit that capacity, right, to imagine that COVID was going to be the new normal.”

Operationally, the company was in disarray. The order management system, built on outdated code, caused headaches across departments, particularly in accounting and customer service, where employees had to navigate up to 16 different screens just to access a customer’s history. Engineers, too, were hamstrung, unable to push updates or efficiently run A/B tests. “We have to wait until the end of June to A/B test something that would take 1.5 days at Netflix,” McCarthy lamented.

To right the ship, McCarthy transitioned Peloton to a variable cost model, exiting in-house manufacturing, outsourcing logistics, scaling back retail, partnering with Dick’s and Amazon, and launching a bike rental program (primarily) to clear excess inventory.

“If you look at our balance sheet, you’ll see that the business is not going away, which for a long time was a systemic threat. So, because of that, we’re able to focus on renewed growth … I think you’re going to see significant product innovation in the next two years, which I’m very excited about because we have a real shot at changing the growth trajectory of the business.”

- McCarthy, Q2 2024.

Overview and Business Model

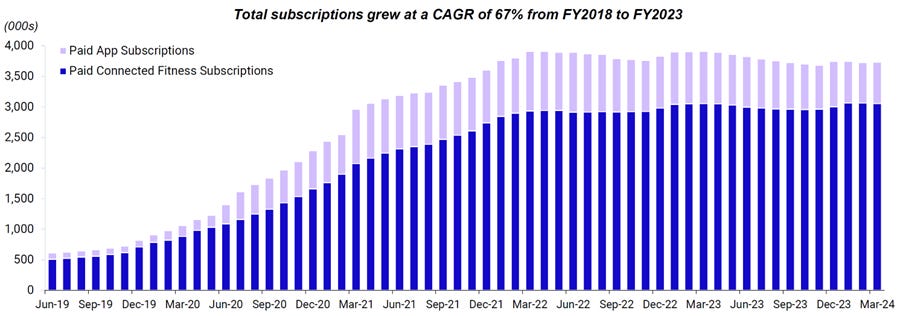

Peloton closed 2024 with 6.4 million members spread across 3.6 million paid subscriptions, including 2.98 million Connected Fitness (CF) and 615,000 digital app subscriptions. A “member” is defined as anyone with access to a paid account who completed at least one workout in the past year. Notably, around 10% of CF subscribers own more than one Peloton product—a clear sign of the brand’s appeal.

While Peloton is making moves into commercial spaces like hotels and campus gyms (we’ll touch on that later), over 90% of its CF subscriptions are held by households. Members are highly engaged, averaging 14 workouts per month per CF subscription in 2024.

Peloton currently operates in five key markets, with the U.S. accounting for about 90% of its revenue, followed by the U.K., Canada, Germany, and Australia. Its distribution strategy combines direct sales with third-party (3P) retail and logistics channels. However, in Austria (and soon Germany), it relies exclusively on 3P partners.

Roughly two-thirds of Peloton’s lifetime sales have come from hardware, with bikes making up about 90% of the units sold. Beyond its flagship products, Peloton offers the Guide, a personal training device, as well as a range of accessories and apparel.

Hardware

Peloton’s hardware pricing, including delivery and setup, ranges from $1,445 to $2,495 for the Bike and Bike+, $2,995 for the Tread, $3,295 for the Row, and $6,000 for the Tread+. The pricing is competitive within their category tiers, though Peloton offers fewer models compared to rivals like NordicTrack, which has eight treadmills to Peloton’s two, and Hydrow, which offers three rowers to Peloton’s one.

To paint with broad strokes, Peloton’s hardware stands out with its sleek, minimalist design, whisper-quiet operation, and premium materials like soft-touch coatings and carbon steel—while many competitors rely on lower-grade plastics and standard finishes.

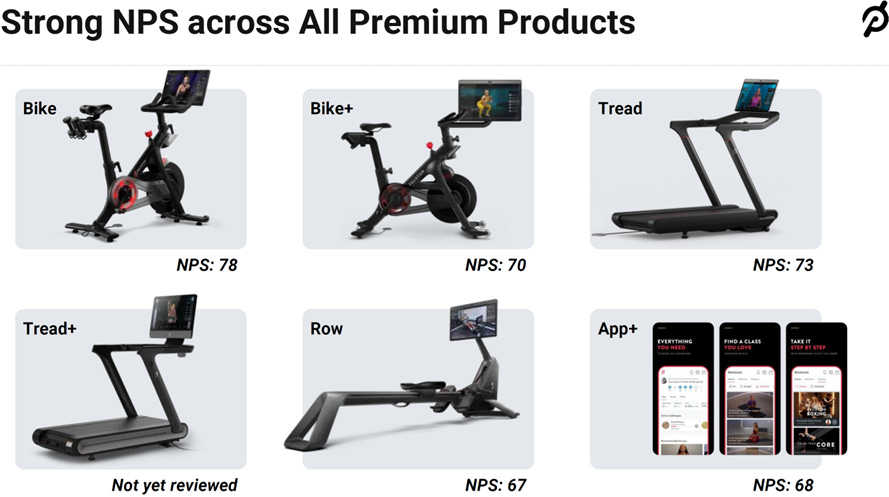

Peloton also excels with its industry-leading software and user-friendly interface, but it’s the content that drives its high Net Promoter Scores (NPS) and fosters deep customer loyalty.

The Tread+ is not currently available outside of the U.S., and the Row is only available in Canada outside its home market.

Content

Peloton streams over 1,000 live classes each month, across 16 modalities in English, German, and Spanish. Its cutting-edge studios in Hudson Yards, NYC, and Covent Garden, London—both located in prime, affluent areas—offer distinct advantages despite their high operational costs.

The cycling studios are the largest, with 39 bikes in NYC and 24 in London. Nestled in two of the world’s most visited cities, they’ve become pilgrimage sites for many Peloton members when traveling. Classes, priced at around $35 per session, fill up very quickly.

This intense demand highlights members’ enthusiasm, especially when they have the chance to meet their favorite instructor—a moment that often leaves them starstruck. It’s more than just fan service; it’s a well-oiled loyalty engine that reinforces Peloton’s unique place in the fitness world.

Unsurprisingly, the energy in these classes is palpable, even for those tuning in remotely. Features like Peloton’s leaderboard and social tools—like high-fiving fellow riders—amplify the sense of community. But what truly sets Peloton apart is its seamless integration of music, powered by the company’s proprietary platform.

Music, as it turns out, is no small matter. Delivering this perfectly synchronized experience requires securing public performance, reproduction, and synchronization rights—unlike radio stations, which only require performance rights. The result? A finely tuned experience where, when an instructor calls out “Right, right,” your foot instinctively follows the beat, pulling you deeper into the workout. In 2024, Peloton spent $137 million on music royalties, accounting for 25% of its subscription cost of revenue.

Instructors, with the help of music experts, curate playlists for each class, and members often choose sessions based on the music selection. In contrast, many other platforms rely on unsynchronized background tracks—if they even offer music at all—and typically have limited in-studio class sizes, if any. To fully grasp these advantages, take a look at these clips comparing Peloton with its main rival, iFIT, where the differences are striking.

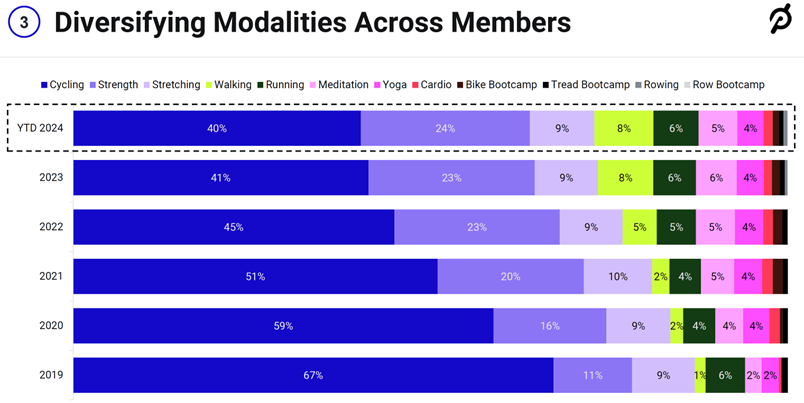

In recent years, Peloton has leaned heavily into non-cycling content, particularly strength training—the most popular form of at-home exercise in the U.S.

Peloton’s focus on high production value, diverse content, and expanding entertainment options1 has resulted in a 75% increase in monthly workouts per CF subscription since 2018.

Subscriptions

Peloton offers three subscription tiers: the All-Access Membership for hardware users at $44 per month, and two digital options—App One at $13 and App+ at $24. The key difference between the digital tiers is that App One limits access to equipment-based classes, while App+ offers unlimited access to all classes, including performance metrics. The company also partners with employers, insurers, and other enterprise clients to subsidize access to both the Peloton App and All-Access Membership for employees and members.

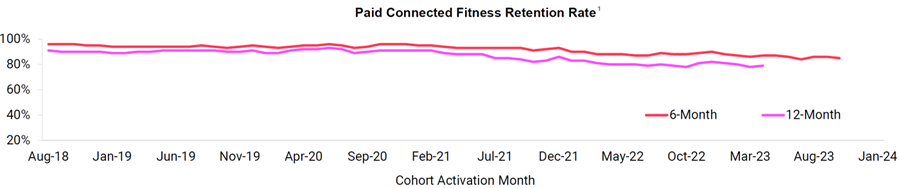

Retention

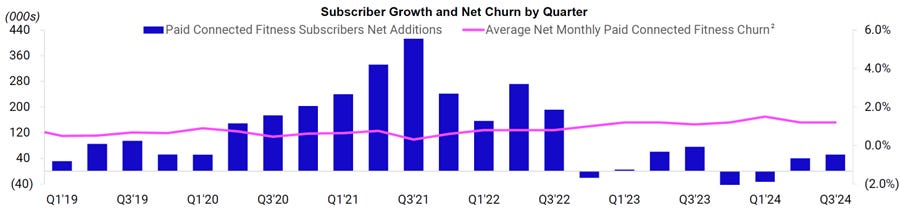

In 2024, the average net monthly churn rate for CF subscriptions was 1.4%, compared to approximately 5% for rentals and 7.7% for paid app subscriptions. The CF churn rate has risen above the five-year average, primarily due to a revenue shift toward higher-churn segments, particularly secondary market subscribers.

Secondary market subscribers show slightly higher churn rates than direct subscribers. As this segment has grown, so has overall CF churn. In response, Peloton has introduced new initiatives aimed at improving the buying and onboarding experience for these users.2

Higher churn has also been observed among cohorts acquired after the initial COVID boom, when Peloton started aggressively targeting non-core demographics, particularly Gen Y and Gen Z—a strategy now seen internally as a misstep and subsequently scaled back.

Competitive Landscape

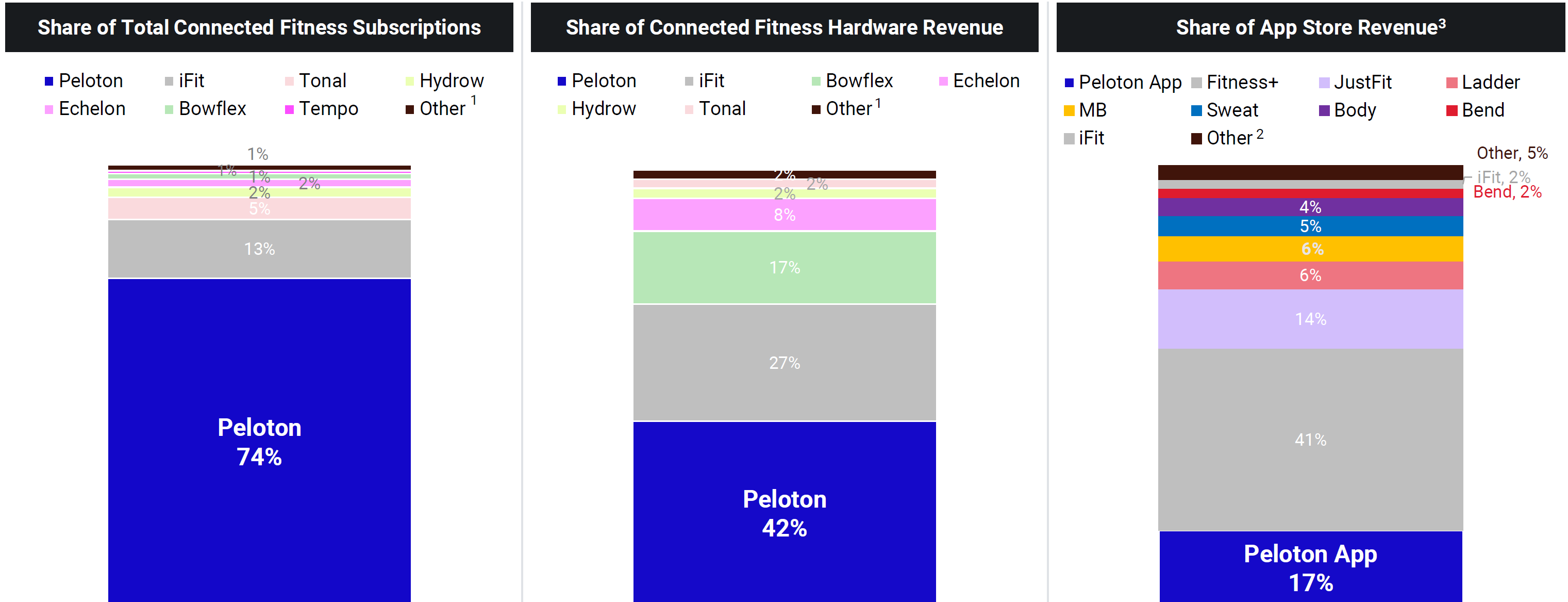

Peloton faces competition from fitness apps, mid-tier and higher-end gyms, boutique fitness studios, and other connected fitness providers. Recall iFIT, its main rival and the parent company of brands like NordicTrack, ProForm, Weider, and Freemotion, which has long been a key player in the industry.

iFIT offers a broader range of equipment, from entry-level to premium, and maintains a stronger foothold in the commercial market, while Peloton has remained primarily consumer-focused. The sharpest divergence, however, is in their subscription businesses—where iFIT has faltered despite the bold projections in its since-withdrawn 2021 S-1 filing.

At the time, iFIT’s engagement was half of Peloton’s, with a churn rate more than double. Yet, iFIT touted its connected fitness platform as “unmatched” and predicted significant market share growth. The reality has been quite different: since March 2021, Peloton has added approximately one million net connected fitness subscriptions and doubled its revenue, while iFIT has lost around 500,000 subscriptions. This pattern extends to other competitors like Bowflex and Echelon.3 Despite steady hardware sales, neither has cracked the subscription model.

Barry McCarthy understood early on that success in hardware was secondary to winning in content and shifted Peloton’s focus accordingly. As he put it in May 2023:

“So, do I want to sell hardware? Or do I want people engaged in the content? I want people engaged in the content. If you want to consume it on our platform, that’ll be a terrific experience. But if you bought somebody else’s hardware, we’d still be delighted to have you.” He added, “If you can afford a Mercedes, great—we’ll take a Mercedes. But if all you can afford is a Ford, then we'd be delighted to sell you a piece of the Magic Kingdom.”

And Peloton has indeed sold thousands of those “pieces of the Magic Kingdom” to users of competitor hardware. Indeed, there’s even a Facebook group called “Peloton Digital App users + Echelon Bike Riders” with over 11,000 members.

What’s Next for Connected Fitness?

Peloton wasn’t the only company to overextend during the pandemic-fueled home fitness boom. Capital flowed into connected fitness like the next gold rush, but the surge was followed by an inevitable correction. Since 2019, Peloton’s main competitors—iFIT, Hydrow, Echelon, and Tonal—raised over $1.5 billion collectively. Yet, as the dust settled, the sector found itself grappling with financial instability and rounds of layoffs. Bowflex, for instance, filed for bankruptcy in May 2024.

With capital drying up, these competitors are likely to lose ground as the industry consolidates. As rivals tighten their belts and cut spending—particularly on high-cost advertising targeting Peloton’s core demographics—Peloton stands to benefit. Less competition for premium ad placements means lower CPMs, making it easier and cheaper for Peloton to reach its most lucrative prospects.

Additionally, it seems inevitable that competitors will pivot toward more open ecosystems—a trend already in motion—allowing seamless integration with third-party apps like Peloton. This shift will be crucial for driving hardware sales, which remain the backbone of their revenue.

Digital App

Peloton’s real competition on the digital side comes from tech giants like Apple (Fitness+) and Google (Fitbit), but as we've seen in streaming, deep pockets don't always guarantee success—just look at Apple TV and Amazon Prime next to Netflix. Apple has been producing fitness content for years, and while it’s decent, it’s not in the same league as Peloton’s. The same holds true for Fitbit. As one former Peloton VP of Content Production bluntly put it: “I know what Apple spends on their content. I know what Peloton spends on theirs. It’s clear which one is really making it.”

Peloton’s content engine, fueled by millions of engaged members, has created a virtuous cycle: top talent flocks to the platform, eager to build their personal brands and land licensing deals. But as Apple Fitness demonstrates, it’s not just about audience size—it’s about the power of the Peloton brand and the doors it opens.

Of course, this begs the question: what happens if Peloton’s star instructors jump ship to Apple Fitness or another competitor? The so-called “instructor exodus,” where three instructors left amid contract talks, did raise eyebrows. But with 59 world-class instructors on board, losing a few is hardly a crisis. Peloton’s connected model, where members invest in expensive equipment and belong to a tight-knit community, adds a protective buffer. When one instructor exited and criticized Peloton, it quickly became clear where members’ loyalties lay—and the content disappeared from the platform.

These dynamics explain Peloton’s dominance in app store rankings and its digital growth potential. But this confidence wasn’t always there. Before its 2023 relaunch, the app wasn’t exactly making waves. Leaked communications from January 2022 revealed one executive’s blunt take: “Our app is terrible.”

Still, Peloton’s app suffers from low awareness—just 6%, compared to over 55% for the Bike. That disparity signals a huge growth opportunity. As McCarthy noted in Q2, “The app is the best product we have that nobody knows about.”

Community

While Peloton’s missteps and controversies have certainly left a mark—though often overstated—it has achieved something few others have: building and sustaining a fiercely loyal, engaged community. This is evident in the presence of at least three podcasts solely dedicated to Peloton, each consistently producing content for several years.

It’s no surprise that Peloton was featured on the popular podcast Sounds Like A Cult in 2023. The hosts, while making playful comparisons to actual cults, noted: “… [Peloton] doesn’t require you to recruit anyone, but you just want to … Once you get hooked, you’re going to want to evangelize it to all your friends … you want them to join because it’s something that changed your life for the better…”

A powerful example of this community spirit was on full display when Peloton Tread instructor Susie Chan participated in the Badwater 135 Ultramarathon, considered the world’s toughest race. A group of Peloton members, known as "Susie’s Striders," organized a relay challenge to support her, ensuring that at least one member was running—on their Tread or outdoors—for the entire 41-plus hours it took her to finish the race. Some even woke up at 2 or 3 a.m. to make it happen.

Few brands have cultivated such dedicated communities around them.

| A guest post by

|