Deep Dive: HDFC Bank (HDB US)

A framework for bank analysis

Welcome back to our subscribers! If you are new, subscribe below for monthly deep-dive research on global stock ideas and other original investment content!

HDFC Bank

Summary

HDFC Bank is India’s largest private bank. The stock has been a tremendous compounder. Despite having always looked ‘expensive’, it has rewarded shareholders with a CAGR of 21.4% over the last 20 years (in USD). HDFC Bank is an option on India’s GDP growth and financialization.

We find that the most important factor one needs to possess to own any stock, but especially a banking business in an emerging market trading for premium to book value, is conviction. With this in mind, we’ll explain why we believe HDFC is a rock-solid banking business by deconstructing the key elements of a bank business model.

We acknowledge that a bank can be a bit of a black box, which is why it’s important for investors to have confidence in not only a bank’s business, but also its culture and management. HDFC Bank has a strong track record of navigating economic cycles through prudent risk management.

The ADR’s share price is at the same level as in June 2019, while the bank’s book value per share is higher by 41%. The best time to buy HDFC Bank has been when it is trading at the lower end of its valuation levels. Today is one of those times. We believe one can buy HDFC Bank for a 45% upside in two years or an IRR of 20%.

Context

Secular ‘plays’ in the Indian banking sector

An understanding of the banking system is important to understand the inner workings of any economy, but especially an emerging economy. Indian banking has had a colorful history. We’ll start from the beginning. Temples used to perform the banking function in ancient India. In the larger society, it was a little more complicated. We know that India has been and still is in many ways divided amongst its regions, religions and castes. There are specific castes for money lenders. Money lenders within other castes typically only lent to their own castes (or below). Mobility was limited so all this lending was very regional. It was easier to shame and collect if they knew the borrower or his extended family. You see, these money lenders understood a long time ago that banking is not a lending business, it’s a collections business.

This is important to understand because, even today, at the local level, a large part of the market is controlled by money lenders. These lenders charge usurious rates but borrowers typically are uneducated or find these money lenders to be more flexible or easier to deal with. It becomes difficult to calculate the exact interest when all you understand is that you have to return your Rs. 2,000 in equal monthly installments of Rs. 200 over 12 months. Easy does it.

After independence, the banking system was a mix of state-owned banks (increasingly being consolidated by State Bank of India or SBI) and banks that were built and owned by Indian industrialists. In 1969-70, decisions were made by the then-government to nationalize the largest private banks. The rationale was that these private banks were not lending to the agricultural and small businesses and were too focused on urban areas (where unit economics worked). After nationalization these banks expanded their business in semi-urban and rural areas even if it was not profitable. Within two decades, these state-owned banks had 91% share of bank branches and 85% share of assets. The balance was shared by smaller private banks and foreign banks such as Citibank or Grindlays. The foreign banks were needed for trade and foreign exchange but were not allowed to open branches. Over time, due to political lending, bad governance, incompetence and misaligned incentives - at all levels - the banking system led by public banks became technically insolvent. Now, the politicians found that without a healthy banking system, it would be difficult for the economy to grow because well...you need credit growth in any modern economy. The authorities then decided to invite private players to start new banks in India. These private banks have since taken advantage of their weaker public peers and consistently gained market share.

There have been two secular plays emanating from this:

Slowly bringing people into the formal banking system

Market share gains by new private banks from public sector banks

Founding of HDFC Bank

HDFC Group, then led by Deepak Parekh, had built a successful mortgage lending business. This group was known for its integrity and competence. HDFC Group applied for a banking license, got one, and HDFC Bank was officially born! Other interested groups were industrialists with convoluted interests, and the regulator was wise enough to reject most of these applications.

Deepak Parekh hired the then CEO of Citibank Malaysia, Aditya Puri, to run this startup bank. Citigroup was known to be a bit of a talent factory in Asia. In hindsight, it was probably the best decision in the annals of corporate India. Aditya led the bank from 1995 to 2020 – a 25-year stint during which, from a standing start, HDFC Bank became the largest private bank in India. Aditya had a clear vision for the bank.

“If we can put together the products and services of foreign banks and the relationships, funding, and distribution of national banks, nothing should be able to stop us”.

-Aditya Puri

During that time public banks had all the branches and foreign banks had the best products (and best clients). Aditya hired the best talent from other foreign banks and used his rolodex to get business for HDFC Bank. As it was a new bank, the tech stack could be built from scratch. No legacy systems!

HDFC Bank, like Microsoft or AWS, had a few years to grab market share and establish first mover and scale-based competitive advantages. There was no real competition! Remember, this is a time when public sector banks had 91% market share. These banks had vast infrastructure, extensive branch network, low-cost deposits, good relationships but very bad products and services. Importantly, they were constrained in growing their balance sheet due to low capital levels.

HDFC Bank’s strategy was to penetrate public bank clients and then increase their share of wallet. Initially, the bank gained accounts from the big industrial houses, public companies, and government at all levels. These institutions were served by public banks and found HDFC Bank’s services markedly better. After that, they went after employee accounts, then supplier accounts, then distributor accounts and on and on. Not only did this really help with stickiness and scale, it would also be key to risk management.

The easiest way to grow a bank is to write big cheques to big clients. Incentives can further exuberate this behavior. But easy is seldom profitable. Profitability comes from consistently doing small things well. Aditya and the team used their Citigroup relationships to get HDFC Bank some corporate business. It was important to build some scale as these profits would be required to do what they really wanted to do – build a retail franchise. Slowly but steadily HDFC Bank started building a branch network that was needed to attract deposits. With their technology, they also built products and processes for granular retail lending.

Accelerating the flywheel

The raw material in this business is capital. A new bank that is growing at a rate much in excess of its return on equity (ROE) needs to raise capital in order to sustain that growth. HDFC bank had to raise capital many times but always raised capital at a premium to book value so these capital raises were always accretive to book value per share. In initial years, a premium valuation is a big advantage as it lowers the cost of (equity) capital.

With this capital, methodically, it kept on building branches; it kept adding products; it kept hiring talent. HDFC Bank was the first credible alternative to public sector banks and had the whole field open to them. They could get the best clients, secure the best retail locations for branches, and hire the best talent before other private banks could find their footing. There are switching cost advantages in the banking business. Customers had a good reason to add HDFC Bank to their roaster but no good reason to add another private sector bank unless it offered juicy incentives.

In order to make its flywheel run even faster, HDFC Bank merged with Times Bank in 1999. The big merger happened in 2008 when HDFC Bank acquired Centurion Bank of Punjab and greatly expanded its presence in North India. Not a roll up; just strategic acquisitions to gain regional scale.

India, along with other emerging markets, went through a bit of a boom from 2003-2008. The country was not directly affected by GFC. Government stimulus since meant that there were a lot of corporate and infrastructure projects to be financed in the country. While its peer drooled over lending to unprofitable infrastructure projects run by shady promoters, HDFC Bank steered clear. The Indian banking system has had rolling crisis since 2012 where bad assets in the system have overwhelmed most of HDFC Bank’s peers. System Non Performing Assets (NPA’s) were as high as 15-20% of total loans which hampered most banks from expanding their balance sheets. HDFC Bank got another decade of free reign to grow its balance sheet!

Digital Transformation

Starting 2015, digital trends started accelerating in India. The government and RBI introduced the following,

‘Aadhar’ biometric identification system. With this, the government gave a unique identity to each individual in India. This unique identification can be used for Know Your Client (KYC) norms which was always a cumbersome process for financial institutions in India

The government built payment rails called Unified Payments Interface (UPI). This was partly a learning from China and partly from Crimea. US sanctions meant that Visa and Mastercard rails stopped working in Crimea after annexation by Russia and every self-respecting emerging economy policymaker took note.

RBI started granting banking licenses to newer operators which were technology first. Using Aadhar KYC, payment banks could onboard customers with a few clicks. Along with PayTM, foreign operators such as GooglePay and WhatsappPay have been operating in India.

These trends grew exponentially after Reliance Jio introduced its mobile services at rock bottom prices. Now, more and more people in India had access to mobile phones and data.

Aditya Puri was ahead of these trends. Mastercard organized a trip for him in Silicon Valley in 2014 to meet startups disrupting financial services. His conclusion from meeting these companies was that they were not really disrupting banking but were building APIs on top of the existing banking infrastructure. Then he channeled his inner Cathie Wood, and said: why don’t we disrupt ourselves instead of letting these startups disrupt us? This is another example that exhibits Aditya’s brilliance. HDFC Bank started working on its tech stack with 4 major principles:

Reduce turnaround time

Change credit and risk management processes for greater efficiency

Make the customer experience frictionless

Apply AI to the huge amount of data at the bank’s disposal

One of the innovations that came from this was a 10 second loan. Any existing HDFC Bank customer was approved for a loan within 10 seconds based on AI and data. This was further extended to pre-approved loans. A letter would come to a client’s house with pre-approvals for various types of loans which the client could avail as per their needs. No need to apply for anything – frictionless!

The other innovation was ‘bank as a marketplace’. HDFC Bank connected its commercial clients on one side and retail clients on the other on a platform so that they could transact within this closed ecosystem using HDFC cards. This SmartBuy platform has Amazon and Flipkart listed as merchants and as long as customers use a HDFC Bank payment method, they can get additional discounts.

Finally, HDFC Bank redesigned its app to match the best of the fintechs. This app has become a destination app when it comes to financial services. It is the most used banking app in India and 95% of all transactions at HDFC Bank are now initiated online and on the mobile app.

Then, one day, on a fine summer morning, you wake up to these headlines:

‘HDFC Bank and PayTM in payment tie-up'

“The fusion of HDFC Bank’s network, products, and credit appraisal capabilities and Paytm’s technological platform will accelerate digital transformation in semi urban and rural India, while bringing more people into formal banking channels, the two companies said”.

OK. Good.

We acknowledge that there is always risk from technology but banking is a different business. It is highly regulated. Even if something were to happen, it will likely be slow (India is not Brazil!) and an astute investor should be able to navigate that environment.

Transition from high-growth to sound operations and risk-management

Today, things have changed. Most banks have now reserved for non-performing loans. HDFC Bank’s bigger private competitors, such as ICICI Bank and Axis bank have new management teams that are doing their best to institute changes to these institutions to make them more HDFC-like. The largest state-owned bank, State Bank of India, has gotten its act together and upgraded a lot of its technology infrastructure and has been aggressive in retail lending. Newer and more nimble competitors such as Bajaj Finance have emerged that made buy now pay later famous in India long before their western peers found traction. Bajaj Finance has focused and lent to HDFC Bank’s core clients.

The effect of the above is that growth has slowed but not enough to make HDFC Bank unattractive as an investment. Importantly, HDFC Bank is not standing still. While most of its competitors are focused on the more profitable urban markets, HDFC Bank is using its size and scale to expand its network in semi-rural and rural markets. The management believes that they can double the size of the bank with this strategy.

The public sector banks now have a 65% market share in India compared to 91% in 1995. There is still room to gain share!

The most remarkable accomplishment at HDFC Bank has been its low non-performing loan levels. India is a complicated country and it is easy to make mistakes. Not HDFC Bank! It has been able to navigate the economy without a blemish to its income statement. This is possible due to a risk culture. The lending is not done at a branch level. This takes away discretion (the root of all corruption) from the branch manager. The executives responsible for sanctioning loans are also the ones responsible for collections. HDFC has data intensive risk management processes: HDFC Bank lends to the OEM, its suppliers as well its distributors and all their employees and customers. If there is a problem in the ecosystem, it is the first to know. There have been many times in history when its early warning systems have flashed red and it has been able to offload loans to other banks just before they went bad.

Here are the key points from this context:

Long runway: Banks do questionable business when they have no alternatives to grow. HDFC Bank made good loans and grew its assets as it was taking share from public banks and lending in a growing economy. It did not need to do anything dumb. It still has a long runway of growth.

First mover and low cost: Its first-mover advantage as well as its focus on brand network and service meant that it could attract low-cost deposits. These low-cost deposits along with low operating costs (due to tech advantage) meant that HDFC Bank’s margins could be attractive even if it did not do any high yielding risky lending. These cost advantages are being sustained and deepened.

Digital first: While there will always be digital threats, HDFC Bank has been successful in disrupting itself. It has built out a digital bank with products and services that minimize client incentives to switch.

Risk culture: HDFC Bank’s entrenched position in the Indian economy produces superior data that can be analyzed for risk management. Talent has been molded into the HDFC culture where risk comes first. HDFC Bank has a history of low non-performing loan levels even as the economy cycles. Importantly, the buffers are always robust.

Banks are black boxes and it is going to be difficult to know every inch of HDFC Bank’s book. Further, India is an emerging markets and rules and regulations keep changing. This is further accentuated by sell-side who send a ‘world is ending’ note at the slightest of change (we have been at the receiving end and spent countless hours digging into useless details that did not affect the long-term compounding of the bank). We believe if you have a good understanding of their history and culture and believe in the management, enough conviction can be gained to buy and hold this compounder.

"Banking is a very good business if you don't do anything dumb."

- Warren Buffett

One of the concerns people have when investing in compounders is – have I missed it? Are the best years behind? It’s a valid question and the answer in HDFC Bank’s case is yes – you have missed the best days. HDFC Bank used to grow its assets at 30-40% and this has come down to 15-20% in recent years. The formula for HDFC Bank’s growth has been the following:

Growth = GDP Growth + Inflation + Share gain from public banks + unorganized to organized

Growth has slowed due to HDFC’s large size and increased competition. HDFC currently has an 8.5% market share in deposits and 9.6% market share of loans in the Indian Banking system. As a comparison, SBI has a 22.5% share of loans and the public banking system has a 60-65% share. It is important to note that HDFC Bank’s foray into rural and semi-urban markets is recent. By some estimates, these markets are as big as urban markets (and growing much faster). It is likely that HDFC Bank will gain share in this market for a long time.

A part of this slower growth is due to slower growth in India as GDP growth in India has slowed from ~8% to ~5% per year. If GDP growth in India were to turn – watch out!

HDFC Bank’s business

There are a couple of different ways of looking at a bank. While this is not supposed to be a full learn-in on banking businesses, we will try to break down the bank in a way that is easy to understand. We know that ROE = Net Income/Equity. In a bank, the Net Income can be further broken down as follows:

Net Interest Margin (Lending Yield – Borrowing Yield)

+Other Income (Fee income plus gains/losses on balance sheet investments)

-Expenses (people, technology, infrastructure)

-Provisions (loans go bad)

-Tax (government’s share)

=Net Income

Banks would not be so profitable if they did not use leverage. All these deposits and other borrowings are made on a base of equity. If you are Lehman Brothers, you are 30:1 leveraged but if you are a responsible bank such as HDFC Bank, operating under a responsible regulator such as RBI, then your leverage ratio stays ~10:1.

Let's break down each in turn.

1. Net Interest Margin (NIM)

The net interest margin of a bank is the biggest revenue line for a bank and is the difference between the yield it makes from the assets on its balance sheet minus the interest it has to pay on its liabilities.

“A Bank is a business where your assets are your liabilities and your liabilities are your assets”

- Anonymous

Assets

HDFC Bank’s mix of retail to wholesale has typically been 50:50. In FY 21 (ending March 2021), it had a book of US$151 bn out of which US$70 bn was in retail loans. The key insight here is that HDFC’s loan book is very diversified with small loans to many people in many regions such that a few bad loans do not have any material effect on its profitability.

Wholesale can further be divided into corporate and other. These corporate loans (typically half of the wholesale book) can further be divided into term loans (at various maturities) and working capital loans. Most corporate banks in India have gotten into problems when they have lent to long term projects with mismatches in project quality, timing, regulations, or people leading these projects. The sponsoring group usually structures these projects like an option play. They finance the project with minimal equity and make out like bandits if it works. If it doesn't, it’s a ‘bad asset’ for a bank who is forced to work with the promoter to restructure the loan. I was once told by the CEO of a mid-sized Indian bank that a lot of these loans, which are fixed income instruments, actually have equity type risks. HDFC Bank lets the state-owned and other corporate banks do the bulk lending, and only offers working capital loans to these clients.

Other wholesale loans such as emerging corporates, SME’s, commercial vehicles are very retail like and not bulky in nature. Risks are segregated.

The retail book is further divided as follows:

Auto 16%

Personal Loans 22%

Loans against securities 0%

Two-wheelers 2%

Business Banking (SME) 13%

Commercial Vehicles 5%

Credit Cards 12%

Housing Loans 13%

Others 15%

The whole retail book is very granular in nature. No one segment will make or break the bank. Auto loans are a good example. Each dealership has 2-3 preferred lenders that have a seat in the dealership. These lenders typically have a relationship with the OEM and, in most cases, have to be approved by the OEM. Scale, service, relationships, technology, and importantly, data history are all important not just to take a fair share of business within a dealership but also to make sure that it is done profitability.

Here are the other important metrics including the very stable NIMs:

The yields on any loans are affected by the interest rates prevailing in the economy. It is important to note that the loan growth slowed down substantially in 2021 due to Covid-19. India and other emerging markets did not have the option to stimulate their economies by handing out free cash. Everyone had to fend for themselves. HDFC Bank slowed down their loan growth in a material way. This wouldn't be the first time. We observe that HDFC Bank has a history of slowing down or accelerating growth contingent upon its data-dependent outlook.

There is another important nuance here that needs to be appreciated. According to regulations in India, all banks have to maintain lending to certain weaker sections of the society. RBI mandates that these loans should not be less than 40% of a bank’s loan book. Needless to say, a bank that can lend to this section of the society profitably has a huge structural advantage. HDFC Bank actually makes money on its priority sector loans while most other banks do not and cross-subsidize this part of the book with more profitable parts of their book. This makes an enormous contribution to maintaining HDFC Bank’s NIM.

NIM’s are much higher for retail loans than wholesale loans. At the margin, NIM’s decline as wholesale loans grow faster than retail loans (as has been the case over the last 12 months) and increase when retail loans grow faster. HDFC Bank’s NIM has declined as it has been cautious in retail lending which, according to the last conference call, has inflected and, should start reverting back to its normalized average.

Liabilities

A bank typically funds itself with savings deposits, time deposits, debt, perpetual debt, preferred equity and equity. Each of these have a cost-benefit. They key insight here is that HDFC Bank has access to low-cost deposits due to which it has a cost advantage. If banking is only looked as a commodity (in India it is not) then HDFC Bank would be first quartile on the cost curve.

The best source of funding is current accounts and saving accounts deposits – also known as CASA. These are working capital balances for businesses and individuals where clients do not care about yield but the services provided with the account. There are infrastructure and technology costs here, but very little capital costs. A bank with a higher CASA ratio has a lower funding cost and obtains the key raw material cheaper compared to peers. Trust, a big branch network, and technological superiority are typically needed for a bank to keep a high share of CASA accounts.

The next best source is time deposits where a bank incentivizes deposits with higher yields as long as clients keep their capital in the account for a fixed time period. These deposits help the bank match their assets with their liabilities. All other sources of funding come at a higher cost.

HDFC Bank has the following mix of funding:

As we see, a very high-quality funding structure with most of it coming from deposits (and not debt or other instruments) and within these deposits a high CASA contribution. It is precisely due to this low cost and stable funding that high quality banks do not need to go out on the risk curve when it comes to lending and can still maintain good margins. A 50-bps difference in funding costs with the same yield on assets will cause a proportional decline in NIM and a much higher decline in ROA and ROE due to operational and financial leverage.

2. Other Income

Other income is about ~30% of total income. Fees and commissions in turn are ~70% of other income. In essence, out of every $1 HDFC Bank earns in income, $0.70 comes from NIM (Yields on assets – yields on liabilities) and $0.30 comes from fee income. It is important to remember that, theoretically, this other income does not require balance sheet capacity.

HDFC Bank is the largest credit card issuer and merchant acquirer in India. It has a 23.6% market share with SBI Cards at 19% and ICICI Bank at 17.6% (top 3 is 60%!). Further, led by its high quality and more affluent client base, HDFC Bank has a 29% spend share as average spend per card is higher than most other banks. Importantly, the penetration of credit cards remains low in the country as they form around 6.5% of the total cards. There is a massive runway!

Lately, a large part of fees have been coming from distribution. HDFC Bank is using its vast branch network to sell life insurance and asset management products. India has low penetration of these products and a very young population. There is a long runway here!

Fees and commissions have had a 17% 10-year CAGR. This has been lower than 10-year NIM CAGR of 20%. A part of the reason is that while fintech and competition has not been able to disrupt HDFC Bank, they have caused a pressure on pricing. We think most of this reset is now in the books.

In December 2020, due to technological problems (we will discuss later), RBI imposed a ban on HDFC Bank on issuing new credit cards. This ban was lifted in August 2021. This has partly been a reason for negative market sentiment and slower growth. As this is now resolved, we believe HDFC Bank will be back to its growth mode.

In addition to credit cards, HDFC Bank makes fees on cash management services, banking charges, distribution fees (from selling investment products), debit cards, FX, custody, among other services. Very little of its other income comes from trading or other securities on the balance sheet. This is a key difference in Indian banks and HDFC Bank in particular and their western counterparts.

As per RBI regulations, banks have to invest a portion of their assets in government securities (a roundabout way of funding the government!). These securities can have mark to market losses depending on interest rates going up or down and contribute positively or negatively to other income.

3. Operating Costs

Banks have similarities with retailers. You open a branch, build a ‘supply chain’ network, populate the branches with employees to service clients, and sell stuff. A high-cost branch may not be profitable due to lease costs and a low-cost branch may not be profitable due to low throughput. These banks have to be connected to regional offices and files and data have to move back and forth in a seamless manner. All this activity has to be performed and recorded without missing a rupee. It is difficult to accomplish this without technology (although I have seen stacks and stacks of paper in the offices of some public sector banks and they somehow manage to balance their books!). A robust core banking platform is needed. In today’s digital world, this core needs to be open enough such that newer technology can be added as required.

A lot of legacy western banks operate on very old systems. Some of them were written in languages that are not in widespread use today (the IT services sector in India is a big beneficiary). A technology executive described upgrading core banking systems as doing an engine replacement while mid-flight. Due to this, they are not very popular. Typical US banks operate at a 50-60% Cost to Income ratios. HDFC Bank operates at 37%! HDFC Bank has had the advantage of starting its technology stack from scratch. Its core banking system was I-Flex which was eventually acquired by Oracle. HDFC Bank also benefits from all the Indian talent in IT services.

How does HDFC achieve it? Again – doing the small things well. If we look at efficiency metrics such as revenue/employee, employee/branch, profits/branch and the like – all ratios are first class.

The important thing to appreciate here is operating leverage. HDFC Bank has close to 5,500 branches. Branches are high cost and the amount of branches a bank can add is directly proportional to the existing branch infrastructure. If you add too many branches, your cost to income ratio will go for a toss as these branches will take some time to mature. HDFC Bank has a first mover advantage. It was one of the first private banks to build branches in more affluent urban areas and lock in the best customers. In the last 5 years, it has replicated this strategy in semi-urban and rural areas. Other private banks find it too cost prohibitive to enter these regions but HDFC Bank has the scale and scope to enter this business. As it is the first mover in semi-urban and rural areas, like it was in urban areas, it is likely to gain the best business available in these regions. The second player just cannot have the same efficiencies.

Lately, there have been problems when it comes to technology. There have been a lot of outages and customer complaints. This culminated in RBI banning HDFC Bank from issuing new credit cards. Perhaps this was the result of too much growth? HDFC Bank has 45 mn customers! Or perhaps this was to meet ambitious targets on cost to income ratios and the bank took some shortcuts? We think a bit of both.

The lender is now revamping its technology infrastructure by making large-scale investments, wherein it is bringing new talent, getting into cloud-native stacks, and working with strategic partners for better products and services. The slap on the wrist by the RBI was perhaps all that was needed and HDFC Bank FY21 annual report is full of evangelical technological ambitions. We believe cost to income ratios have likely stabilized and any further gains from operating leverage will likely be further reinvested into technology.

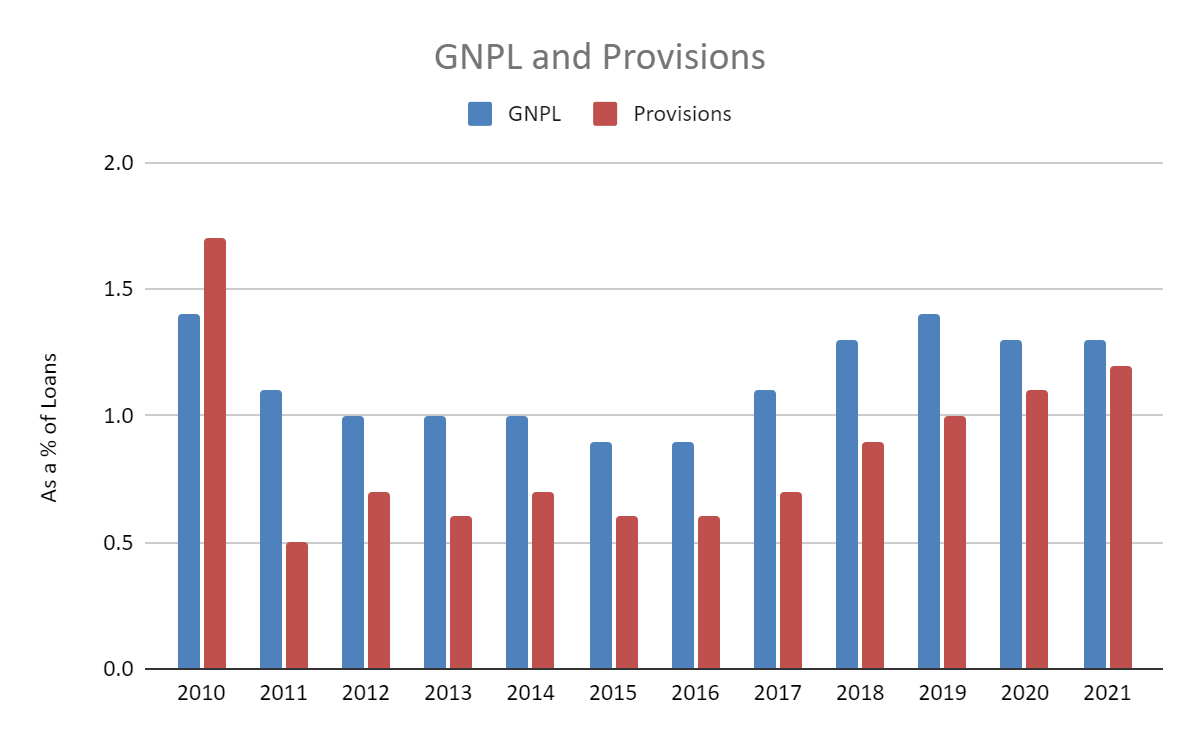

4. Provisions

A loan loss provision is a cash reserve a bank creates to cover problem loans. When a borrower defaults on a loan, the bank has to recognize that loan as a non-performing loan (NPL). It is important to note that the goal is not to have zero NPLs. The goal is to have a good blended ROE and work backwards to the NPL’s that can be tolerated to achieve the said ROE. Every line of business is different.

"Adventure is the life of commerce, but caution is the life of banking."

- Walter Bagehot

For example, HDFC Bank’s mortgage book has lower NIM’s but also lower operating costs and lower NPL’s. The recovery is very high if a loan goes into default. HDFC Bank is probably making close to 12-15% ROE on this business over a cycle. Credit card loans, on the other hand, have very high NIM’s, high operating costs and high NPL’s without the ability to recover much monies. On credit cards, ROE is likely to be 20-25% over a cycle with the assumption that the normalized level of NPL’s is high. On a separate note, subprime lending got a very bad name in the GFC but if not taken to the extremes, it is just lending that is done at a higher yield with the expectation of a higher NPL. Nothing wrong with it.

Provision accounting can be tricky! RBI, the regulator, asks banks to maintain coverages in different buckets which depend on NPL’s meeting certain criteria. I believe understanding these is important and I would elaborate on this if this report was on ICICI Bank or Axis bank which have had high NPL’s in the recent past; but for HDFC Bank it is not important. The bank has robust risk management practices, due to which its NPL’s have remained very stable. As we mentioned above, HDFC Bank has superior data with its tentacles in all parts of the economic ecosystem. It uses this data to manage NPL’s to a reasonable level. More importantly, it always maintains reverses that more than cover its NPLs.

HDFC Bank has come out mostly unscathed from the various crises experienced by the Indian Banking system. During GFC, ICICI Bank almost went under but it was not a big event when it came to sector NPA’s. Both the public and private sector banks were in decent shape. For HDFC Bank, it was a normal cycle where it had to provide for potential bad assets but really accelerated it growth as other banks were affected a lot more.

The problems, as mentioned above, came after 2010 when a lot of the project loans sanctioned by public and private sector banks went sour. The banks were slow to recognize these loans as bad assets and went on rounds and rounds of restructuring. Raghuram Rajan, the then RBI governor sanctioned a report which showcased the real numbers; with NPA’s at some public sector banks as high as 20%.

Why has HDFC Bank been able to do so well? The risk culture plays a big part. It permeates all levels of the organization. Process led lending with strict checks also plays a part. The biggest reason, I believe, is the granular nature of lending. The auto sector can have problems in North India but this is such a small part of the overall book with many small individual loans that it does not affect credit quality. For HDFC Bank to have a real NPA issue there has to be a systemic crisis – across asset classes and across geographies.

It is remarkable that HDFC Bank came unscathed from Covid-19. Both retail and commercial clients were affected due to the pandemic.

There is one caveat when it comes to loan losses. In the past, HDFC Bank was able to offload risk to other banks when it saw its early warning system flashing red. This will be increasingly difficult due to the size of the bank.

5. ROA and ROE

Taxes are taxes. Leverage ratio at HDFC Bank has averaged 9x and have ranged from 7-13x. This has resulted in the following ROE profile.

ROA is the key metric here when looking for consistency. ROE can fluctuate due to leverage.

We like to look at leverage on a very simple assets/equity basis. The regulators look at it in a more complicated way with capital ratios. Each component of asset is given a risk weight, and numerator becomes risk weighted assets which is each asset multiplied by its corresponding risk weight. For instance, a mortgage loan would have a lower risk weight than a credit card loan. This did not work well for Lehman Brothers and is not likely to work in future crises. Only common sense will.

Importantly, during most of its history, HDFC Bank’s growth was much higher than its ROE due to which it had to issue equity in order to finance this growth. These capital raises have become less frequent and we believe HDFC Bank is self-sustaining at current levels unless growth really accelerates.

Tier I and Tier II ratios derive from these regulated capital calculations. HDFC has always maintained healthy ratios. Currently, Tier 1 ratio (really high-quality capital) is at 17.3% and Tier 2 ratio is at 1.2% for a total capital adequacy ratio of 18.5%. HDFC Bank has generally raised capital when its Tier 1 ratio comes close to 11-12% and management has an optimistic view of future growth.

Management & Ownership

HDFC Ltd. incubated HDFC Bank and currently owns 22% of HDFC Bank. It is also a listed company and is involved in mortgage lending. HDFC Ltd. and HDFC Bank have an agreement on mortgage lending where HDFC Ltd is the sole processor of mortgage loans between the two. HDFC Bank takes a fee of 1.1% for originating loans (originates ~26% of all HDFC Ltd. loans) and then keeps a certain portion of those loans on its balance sheet – to be serviced by HDFC Ltd.

In addition, there are rules in India which limit foreign ownership in individual banks. HDFC Ltd. is majority foreign owned due to which its ownership in HDFC Bank is considered foreign ownership. Due to this, HDFC Bank sometimes trade at a premium to its quoted stock price. Its ADR – HDB – always trades at a premium to the underlying. The ADR consists of three shares of HDFC Bank.

The other fallout from HDFC Ltd. ownership is that HDFC Bank does not own its asset management or life insurance arms unlike other banks such as Kotak Bank (HDFC Ltd does). Although, distribution, and not manufacturing, has proven to be more lucrative, HDFC Bank would likely have been even more highly valued had it owned those assets.

HDFC Bank was led for a long time by Aditya Puri – its visionary and very capable leader. He left due to RBI regulations that do not allow executives beyond 70 years of age to lead a large bank. HDFC Bank’s long time CFO – Shahi Jagdishan – has taken over as the new CEO. The board ran a process and looked at both internal and external candidates and there was a fair but of turmoil during this succession. Shahi is capable but he is not Aditya. Shashi also benefits from the fact that the twin strategies of digital and semi-urban/rural are now in motion —and all he has to do is channel his inner Tim Cook and execute. I think it is too early to judge his tenure but HDFC Bank has a strong board with representations from HDFC Ltd. - just in case.

Further, HDFC Bank has seen some brain drain with many of its executives leaving to take up better positions at other financial instructions. HDFC Bank has maintained that it is a process-oriented bank and that a few individuals leaving is not going to change its trajectory. We agree, but the trend needs to be watched.

The bank has low base salaries and ties ~50% of compensation for mid-level executives and up to variable compensation including stock-based compensation. This has its positives and negatives but we do not find any concerns here.

The underlying point remains – HDFC Bank has a very strong risk culture that, along with its entrenched competitive advantages, should see it do well for a long time.

Valuation

There is no DCF for a bank. The market has been fairly efficient in valuing HDFC Bank. We look at the bank on a Price to Book ratio.

The bank was valued at 5-6x P/B during its high growth years in the 2000‘s, then it reset to 3.5-4.5x in the 2010’s and is currently in the 3-4x range. The multiple was correlated with growth and ROA and not ROE. There were many times when the bank had low ROE’s due to low leverage and the market looked through that. It is also important to mention that a premium valuation in this sector is a competitive advantage as it leads to low cost of (equity) capital.

With perfect hindsight, the right strategy would have been to accumulate HDFC Bank shares as it traded at the lower end of its P/B value range.

Here is how the BV (in INR) is likely to evolve over the next few years and related P/B.

2021 2022 2023E 2024E

BV 370 430 505 597

Growth 16.22% 17.44% 18.22%

Stock Price 1,440 1,440 1,440 1,440

P/B 3.89 3.35 2.85 2.41

Target P/B 3.5

Target Stock Price 2,090

Upside 45.10%

IRR 20.46%

It is important to note that year end in India is in March so when we say 2022, we mean year ending March 2022. The above growth in book value is based on 15-20% increase in the loan book with a corresponding increase in net income. No operating leverage assumed but financial leverage will increase which will give HDFC Bank a slightly higher ROE.

For ADRs, one has to multiply the INR stock price by three and divide by the INR:USD rate. The ADR’s have always traded at a premium and this premium is currently at 10% which is on the lower end of its historical trading range. With the same 10% premium, the upside target for the ADR’s in two years is US$92 per share compared to current price of US$63 per share. The premium can be much higher than 10% (has been as high as 25%) in which case the upside target should be above $100 per share.

We believe current stock price has a margin of safety:

Growth can surprise to the upside: HDFC Bank did not grow much in the recent past. We believe this has been a prudent decision. Expect HDFC Bank to ramp up its balance sheet as soon as it sees green shoots. The RBI ban on card issuances further hampered growth. HDFC Bank has guided to adding 300,000 cards as this ban was lifted.

Capital outflows now; inflows later: Bank stocks in India are being sold as foreign investors are selling emerging markets as well as Indian securities due to FED taper. We observe that historically capital has flowed in and out of India based on macro events. It is profitable to be a contrarian investor and invest when the tide goes out. We believe 3 rates in 2022 are likely priced in; anymore and there are other things to worry about! Also, USD has been strong but INR has held up. India is in a decent fiscal position and INR should do better in a weaker USD environment – if one finally materializes.

HDFC Bank is an option on India. India is the last large emerging market. It is always two steps forward and one step back but the direction has clearly been onward and upward. We believe it is important to be nimble and bet on India when valuations are discounted.

HDFC owns HDB Financial and HDFC securities. HDB Financial services is a non-bank financial (NBFC) and is used as a mercenary vehicle to keep other NBFC competition in check (NBFC’s and their regulations is another full report!). HDFC securities is their brokerage arm. These assets are conservatively worth INR 50-70 per share and have not been included above.

Beyond 2024, the stock price can compound close to growth in BV/S which should be above 15%. Again, it is not the 20-25% compounder that it used to be, but it should still do well over time. The big risk remains a recession or a market event, in which case, it will likely be sold along with other securities. It is important to remember that HDFC Bank accelerated its growth after GFC as other banks were badly hurt and not in a position to grow their balance sheet. A similar situation will likely materialize if you were to hold HDFC Bank over a full cycle.

Depending on your investment philosophy, time frame and risk appetite – Kotak, ICICI and Axis are all investable among the large private banks in India but we believe that, at the current juncture, risk-reward for HDFC Bank is better than most.

Disclosure: The author and his firm own a portion of HDFC Bank through a position in its common shares.

Great insights about this giant of a business

Can you do similar for HDFC?